Around 43 million Americans owe a grand total of $1.7 trillion on their student loans and unfortunately, this number is projected to increase to roughly $2 trillion by 2022.

We all know $1.7 trillion is a massive number, and it’s important to recognize it as what it truly is: a crisis. The weight of student debt permeates every aspect of our lives.

This shouldn’t scare anyone away from their dream of pursuing a college education, but it is crucial to evaluate the vast impact of the crisis in which we’re living.

Here’s What You Need to Know About How the Student Debt Crisis Affects You:

Economic Impact

Student loan debt impacts more than just the individuals desperately praying for their payments to disappear.

While there are various ways student loan debt impacts the economy, we’ll focus on three ways that impact the college student and recent graduate demographic most:

- Shifting the economic power away from students and recent graduates

- Lowering the rates of homeownership

- Shifting timelines of typical life milestones

Shifting the Economic Power Away from Students and Recent Graduates

Since the 1980s, the cost of a college education has increased rapidly. A degree that cost roughly $53,000 in 1989 now costs around $104,000. The worst part? Wages haven’t increased at the same rate. This makes it harder and harder for college graduates to pay back their student loans.

As a result of this, students are increasingly disempowered when it comes to investing in a college education. Students hardly benefit from a rise in the cost of education, and rather, lenders, investors, and universities do. This leaves students in a tricky position, often forced to choose between taking out loans for a stronger education or opting for a lower-cost option that feels like less of a fit.

Lowering the Rates of Homeownership

Between 1970 and 2017, the rate of homeownership for Americans aged 20-34 has dropped nearly 10%. While there are various contributors to the drop in homeownership, the student debt crisis is a central factor.

To put it simply, holding an abundance of student debt prevents people from purchasing real estate. Knowing that you have upcoming loan payments can prevent you from being able to save for a down payment on a new home, or from getting into another monthly payment with rent.

While this isn’t as applicable to current college students, it is a large concern for almost everyone’s long-term goals (while it was nice during COVID, few people plan to live at the ‘rents’ place forever). Whether you plan to sell your first home and make a profit or leverage the equity for other expenses, homeownership is a sound financial decision. Not only does it mark a step in fully embracing one’s independence and freedom as an adult, but it helps support the long-term goals of both the individual property owner and the surrounding community.

Shifting Timelines of Typical Life Milestones

Regardless of any internet memes you see poking fun at the differences in generations, there are stark differences between today’s college students and those in our parents’ generation. Due to the increase in student loan debt, current borrowers are (practically) forced to delay traditional life milestones such as purchasing their first car or home, getting married, having children, and even retirement.

Roughly 21% of young millennials are waiting longer to get married and another 21% are delaying having kids due to their student debt. What may be most concerning is that roughly 40% of younger millennials are putting off saving for retirement. While perhaps not a pressing issue at a young age, this does raise concerns for the ability to retire down the line and could impact future generations as they prepare to support the generations before them.

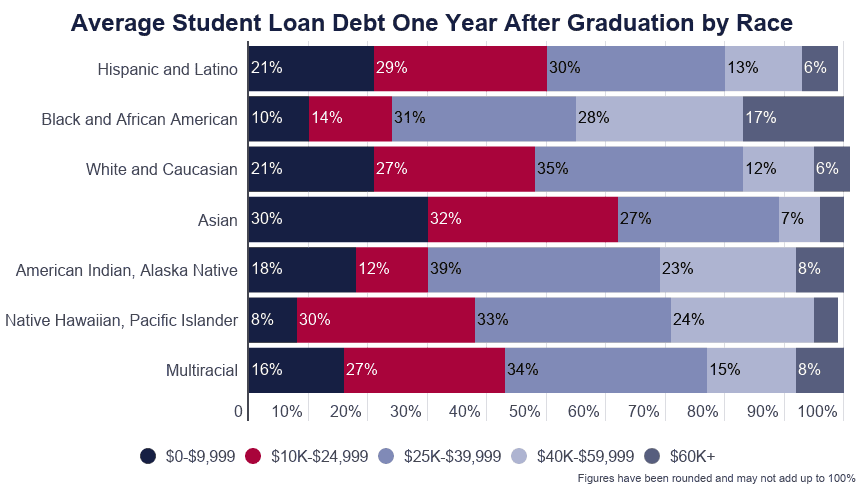

Inequality Impact

There is substantial evidence highlighting the various disparities in the amount of student debt accumulated across racial and ethnic groups.

According to EducationData.org, “Black and African American college graduates owe an average of $25,000 more in student loan debt than White college graduates.” While this figure is important to understand, we must consider how this impacts the milestones we previously discussed.

The impact of student debt goes well beyond the payments and impacts how people engage in the world around them. This is crucial to understanding how deep the inequalities created by student loan debt truly go when left unchecked.

Hanson, M. (2021, June 9). Student Loan Debt by Race [2021]: Analysis of Statistics. EducationData.

Mental Health Impact

If you are a current student or recent graduate, you may be one of the individuals already feeling the mental health impact of student loan debt.

Psychologists have studied the relationship between student loan debt and mental health and have concluded that “student debt has been linked to depression, anxiety, and even thoughts of suicide.” This oftentimes comes from the feeling of being stuck or stagnant in one phase of life, or circumstance, due to one’s student loan debt.

While this doesn’t mean that everyone with student loan debt will experience mental health issues, it is becoming increasingly prevalent. In a survey of college counseling directors, 95 percent said that significant psychological problems are a major, increasing concern for their students

Currently, 1 in 4 young adults between the ages of 18-24 have a diagnosable mental illness. However, we can expect this number to worsen should the student debt crisis continue growing at its current rate.

What Can We Do About the Debt Crisis?

It may feel like we just dropped an absolute bomb on you, and in some ways, we probably have. The student debt crisis is serious, and we do need to think critically about how we can repair such a broken system. With that said, there are positive things happening to fix it.

Politicians are Recognizing the Crisis

More and more politicians are coming forward and recognizing the vast impact of the student debt crisis and sharing their plans to address it.

Acts are Being Proposed

Acts such as Elizabeth Warren’s Student Loan Fairness Act have been proposed to alter and improve the interest rates tied to federal loans.

Schools are Stepping Up

Many universities have announced plans to provide free or low-cost education to low-income students. For example, the University of Michigan created their High Achieving Involved Leader Scholarship to provide a 4-year education free of tuition and fees to qualified low-income students.

Big Tech is Getting Involved

Major tech companies, including Google, Amazon, Microsoft, and IBM, have started offering their own certification programs for a fraction of the cost of a traditional college degree. Their goal is to create standardized skillsets and equip students with the essential skills they need to get a job in high-paying, high-growth career fields. Best of all, the programs do not require a degree or any prior experience to be eligible.

Sparrow is Here to Help

If federal student loans don’t cover your education costs, a private student loan could help. We want to help you find the loan that fits your needs best, saving you both time and money. With Sparrow, you can compare personalized offers from multiple lenders to find the right student loan for you.

- Multiple lenders compete to get you the best rate

- Get actual rates, not estimated ones

- No impact on your credit score

Leave a Reply