You’ve exhausted all of your scholarship, grant, and work-study options. Now, it’s time to start considering student loans to cover that last mile of financial need.

When you look at your student loan options on paper, they may seem suspiciously similar. However, there are various elements to loans that can make them drastically different.

In this article, we’ll break down the key components that make up student loans and provide some helpful tips to ensure you’re getting the best loan possible.

What Is the Difference In These Loan Offers?

If you’re comparing multiple loan offers with the same principal balance, consider the following:

- Federal vs. Private Loans

- Eligibility Requirements

- Annual Percentage Rate (APR)

- Fixed vs. Variable Rate

- Repayment Options

- Monthly Payment

- Repayment Terms

- Grace Period

- Cosigner Release Policies

- Forbearance

- Lender Benefits

- Total Cost

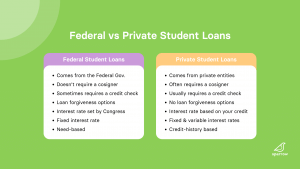

Federal vs. Private Loans

Student loans come in two main forms: federal and private.

Federal student loans are issued by the federal government. Private student loans are issued by banks and other financial institutions.

When comparing a federal loan against a private student loan, it’s important to consider elements beyond their interest rate. For example, federal student loans typically have greater benefits than private student loans.

No Cosigner vs. Cosigner

Federal student loans do not require a cosigner whereas private student loans often do.

Loan Forgiveness vs. No Loan Forgiveness

Federal student loans have the potential to be forgiven through federal loan forgiveness programs. Private student loans, however, do not have loan forgiveness options. If you opt for a private student loan, you will forgo loan forgiveness benefits.

Greater Repayment Options

Federal student loans typically have greater repayment options than private student loans. While private student lenders do offer a wide variety of repayment options, there are some that are exclusively offered for federal student loans. For example, federal student loans have various income-driven repayment options. It’s important to consider how you plan to pay back your student loans when choosing between a federal and private student loan.

Eligibility Requirements

There are a variety of ongoing eligibility requirements when it comes to both federal and private student loans. For example:

SSN Requirements

In order to be considered for federal student loans, you must have a Social Security Number or an Alien Registration Number. If you are concerned about your Alien Registration Number expiring, you may want to select a private student loan that does not require proof of this information. You may be asked to recertify your Alien Registration Number year over year to secure more financial aid.

State Requirements

Some private student lenders require borrowers to live in specific geographic areas. If you anticipate moving or do not have a residential address in that specific area, you may want to select a different loan option. Be sure to read the fine print about state requirements when comparing two loan offers.

Enrollment Status

Different lenders require different levels of enrollment to be an eligible borrower. Federal student loans require borrowers to be enrolled at least half-time to receive aid. On the other hand, some private lenders require at least half-time enrollment while others require borrowers to be enrolled full-time. If you anticipate dropping below full-time status, you will want to compare lenders’ policies for eligibility based on enrollment status.

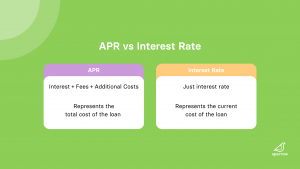

Annual Percentage Rate (APR)

APR, or Annual Percentage Rate, is the annual rate of interest charged to borrowers including any fees and additional costs. Note that APR is different from interest rate as it includes the fees and additional costs, as where interest does not.

APR is written as a percentage and represents the amount of the principal you will pay each year. In other words, this is the amount you would be “charged” each year for borrowing the money.

APR is typically perceived as one of the most, if not the most, important element of a loan. However, before simply choosing the loan with the lowest APR, be sure to compare other aspects of the loan such as fixed vs variable rates, the repayment term, and monthly payments.

If you’re getting caught up on the student loan lingo, check out our Glossary as it might help you understand this article better.

Fixed vs. Variable Rate

Interest rates on private student loans will either be fixed or variable.

Fixed interest rates will remain the same throughout the life of the loan. This means that the “cost of borrowing” the money will always remain constant throughout the lifetime of the loan. For example, if you choose a fixed interest rate loan with a 5% interest rate, it will stay at 5% until you’ve paid it off.

Variable interest rates will adjust over time in response to changes in a financial market index known as the London Interbank Offer Rate, or LIBOR. (Don’t get too caught up in what LIBOR is or how it works. Just know that changes in LIBOR result in changes to your loan’s variable interest rate.) This means that the cost of borrowing may shift over time and is totally out of your control.

There are pros and cons to both fixed and variable interest rates.

Fixed Rate

Pros

- Remains the same each month allowing you to budget accordingly

- Best for people with stable but tight finances

Cons

- Can start higher in comparison to variable interest rates

Variable Rate

Pros

- Tend to start lower in comparison to fixed interest rates

- Good for people who plan to pay their loan off quickly

Cons

- Riskier for borrowers since the rate can change every month

If you’re willing to stomach the month-to-month volatility, a variable interest rate could be a good option for you. If not, we recommend sticking with the more predictable option, a fixed interest rate.

Principal

Principal is the amount of money you borrow when you take out a loan. While you’re in school, you cannot borrow more than the total cost of attendance. Your school’s financial aid office will certify the loan to ensure that your loan does not exceed the cost of attendance.

When comparing loans, you’ll want to pay close attention to how much the lender is willing to offer you. For example, if you need $30,000 to pay for the remainder of your tuition bill, but the lender only approved you for $20,000, that loan may not be the best fit.

Repayment Options

Federal and private student loans will have different repayment options. If you are deciding between taking out more in federal loans or private loans, consider how the repayment options differ and how you plan to pay back your loans.

Remember that the sooner you start making payments, the sooner you will be out of debt. Interest on student loans accrues daily, meaning the longer you wait to start repaying, the higher your total cost. (Note that some federal student loans do not accrue interest while you’re in school, so waiting until you graduate to start making payments may be okay. In general, it’s good practice to start paying them off as soon as you can, but again, always read the terms and conditions!).

Monthly Payment

Before you take out a loan, use a student loan calculator to see what your future monthly payment may be. Depending on the interest rate and repayment period, your monthly payments could differ significantly between loans. Calculating this before you even select a loan will help you in the long run.

Our platform is a great place to start. When you submit a Sparrow application, we’ll show you all of your loan options side-by-side. With each option, we’ll help you compare the predicted monthly payments based on the principal balance and interest rate.

Be realistic about how much money you expect to make after graduating, and ask yourself what would actually make sense financially when weighing your options.

Repayment Terms

Repayment terms include all of the conditions involved in borrowing money from that lender. This can include anything from the repayment period to the interest rate to the penalty fee cost. It’s important to review the loan terms carefully for every single loan you look at. You may discover that one loan would require you to pay back your debt in 5 years which may be a dealbreaker for you.

Pay extra attention to the fees and additional costs. While these are typically reflected in the APR, that may not always be the case. If the additional fees are not included in the APR, they may come as a surprise later on. Thus, be sure to check if these additional fees are included before deciding if one is better than the other.

(You know when you sign up for something and it asks if you’ve read the Terms and Conditions? And you just check it off and go? Yeah, this is one of those times you should really read all the terms and conditions.)

Grace Period

A grace period on a student loan is a time when the borrower isn’t required to make payments. The majority of private student lenders do not require payments while in school or for 6 months after you graduate or leave school. On the other hand, some lenders have a 9-month grace period, and others have no grace period.

Be sure to check if the lender offers a grace period, and if so, how long it is.

Cosigner Release Policies

Because federal student loans do not require a cosigner, this element won’t apply if you are comparing federal student loans. If you are comparing private student loans, however, understanding the cosigner release policy is important.

A cosigner is an individual who agrees to sign onto a loan alongside the borrower. Cosigning a loan can provide the borrower with a lower interest rate or better terms. However, cosigning a loan signifies agreement to pay back the loan in the event that the primary borrower does not.

Thus, many cosigners prefer the option to later be released from the loan, and therefore relinquished from their responsibility to pay back the loan. A cosigner release policy allows the cosigner to be released after certain conditions have been met.

The vast majority of private student lenders have a cosigner release policy, but some do not. If you are comparing cosigner release policies, here are a couple things to look out for:

Income Requirements

Having someone cosign your student loan helps you qualify based on their income, credit history, and financial profile. If you hope to remove the cosigner, you will need to meet those income requirements on your own. Thus, you will need to make sure your credit score is up to par and that you have great enough income to afford your loan payments and other expenses.

Number of On-Time Payments Required

Many private student lenders require the primary borrower to have made a specific number of on-time payments before cosigner release is an option. For example, many lenders require 12, 24, 36, or 48 on-time payments before the cosigner release application is even available. Additionally, fixed and interest-only payments made during school may not count towards this overall number of payments. So, if you plan to release your cosigner after graduation, you may need to wait at least a year to be able to do so.

Forbearance

Loan forbearance occurs when the borrower requests to pause or reduce loan payments for a limited period of time due to economic hardship or other unforeseen circumstances.

Different lenders offer different options for forbearance, ranging anywhere from 12 to 24 months.

While putting your loan into forbearance isn’t ideal and probably not something you plan to do, it’s important to consider when comparing loan options just in case you need it down the line.

Lender Benefits

Some lenders offer exclusive membership benefits to their borrowers. While lender benefits shouldn’t take precedence over elements such as interest rate, it can be a nice added benefit.

For example, some lenders offer free financial planning, referral bonuses, and member discounts to their borrowers. If it isn’t clear what the lender offers, don’t be afraid to ask. Not all benefits will be clearly advertised.

Autopay Discounts

One of the most common lender benefits is an autopay discount. An autopay discount typically provides borrowers with a small interest rate discount for opting in to automatic debit payments. This means that each month, payments will come out of the borrower’s bank account automatically.

Most lenders offer a 0.25% discount, but some offer up to 0.50%. While it may seem small, a 0.25% interest rate discount can save you quite a bit over the life of your loan.

For example, with a loan of $50,000 at a 5% interest rate and a 10-year repayment period, you would pay $63,639 total by the end of the repayment period.

With the same loan and the same repayment period but a 0.25% interest rate discount, you would pay $62,909. While not a massive difference, the $730 saved could be an extra rent payment or vacation.

Total Cost

Because of interest, you will almost never pay back the exact amount you borrowed; you will almost always owe more.

With most private loans, interest accrues even while you’re in school. This means that even if you took out a loan for $10,000 your freshman year, you will be paying back more than $10,000 by the time you graduate or leave school.

Calculating the total cost, or the amount you can expect to have paid at the end of your repayment period, is a very helpful exercise. It will help you see how much you will end up paying in the long run with each of your loan options.

Where to Compare Student Loans

If you’re looking to compare private student loan options side-by-side, Sparrow is the perfect place to start. Simply fill out our Find My Rate form, and we’ll take it from there. After automating your search, we’ll help you compare the options to select the student loan that works best for you.

Final Thoughts from the Nest

The importance of each of these elements will vary from person to person. For example, repayment options might be most important to you, and that may cause you to take a loan with a higher interest rate. On the other hand, securing the lowest interest rate might be most important to you, and that may cause you to take a loan without a grace period.

Taking these elements into consideration will help you find the loan that works the best for you and your educational journey.

When you’re ready to start comparing offers, start here.

Leave a Reply