A great way to reduce your student loan debt is to refinance. An important part of that is looking for a good lender that will offer you good terms. In fact, the best refinance companies are going to give you the best terms. But, what do you even look for? And where do you start?

What to Look for in a Student Loan Refinancing Company

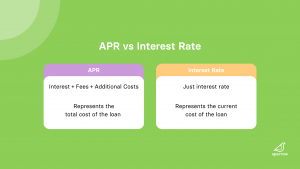

The purpose of refinancing your student loan(s) is to secure a better interest rate or terms.

So, when looking for a student loan refinancing company, you first want to look at their terms and policies. This includes their requirements for approval, the loan terms, cosigner policies, and fees. Here’s a couple things to consider:

Is the interest rate on the loan lower than what you currently have?

Does the lender offer more favorable terms (ie. a longer repayment period) than what you currently have?

Additionally, find out what kind of benefits they offer if any. Do they offer help in the event of financial hardship like the loss of a job? This includes things like forbearance and deferment options.

Make sure the new loan you select offers you a better interest rate or more favorable terms than what you currently have. If it does neither, then refinancing is not an advantageous decision.

Best Student Loan Refinancing Companies

To help you in your search, we’ve made a list of the best student loan refinancing companies.

The Arkansas Student Loan Authority offers loans to Arkansas residents or students who have attended a school in the state. They offer competitive rates and flexible terms to those who qualify. ASLA is best if you either live in or attended school in Arkansas and want competitive interest rates and flexible loan terms.

Best Features

Drawbacks

• Competitive interest rates • Ability to refinance several types of loans • Variety of repayment options • Cosigner release option after 48 months • Offers 0.25% interest rate reduction for opting into auto-debit payments

• Strict residency requirements • Inaccessible for international students

Brazos is a nonprofit lender that provides student loan refinancing to Texas residents. Students must have at least an undergraduate degree in order to take out a refinance loan with them. Brazos offers competitive interest rates and flexible terms to those who qualify. Brazos is best if you are a Texas resident and have at least an undergraduate degree, though the degree does not have to be from a Texas school.

Best Features

Drawbacks

• Work with a nonprofit, rather than a traditional lender • Competitive interest rates • Variety of repayment terms ranging from 5 to 20 years • Generous forbearance options

• Strict eligibility criteria • No cosigner release • No bi-weekly payment via autopay • Students cannot take over parent PLUS loans that parents took out on their behalf

College Ave offers student loan refinancing and is known for their strong customer service, competitive interest rates, and flexible loan terms. For example, College Ave offers nonstandard 6- or 9-year loans, which is unlike many other private lenders. College Ave is best if you want access to good customer service and a flexible repayment term that better matches your budget.

Best Features

Drawbacks

• Strong customer experience • Competitive rates • Choose any loan term between 5 and 15 years including nonstandard terms such as 6 or 9 years

• Limited eligibility criteria • Unclear forbearance policy • Not available to borrowers without a degree, visa holders, or those with parent PLUS loans • Doesn’t allow spousal consolidation loans

Earnest offers student loan refinancing with customizable repayment plans where you can choose your repayment term down to the month. Earnest also has forward-looking eligibility criteria and offers competitive interest rates. Earnest is best if you don’t have a cosigner and want a repayment plan customized to your situation.

Best Features

Drawbacks

• Competitive interest rates • Customizable payments and loan terms • Option to skip one monthly payment every year • Allows biweekly payments via autopay

• Refinancing is unavailable in Kentucky and Nevada • Variable interest rates aren’t available for borrowers in all states • You can’t apply with a cosigner • Student borrowers cannot take over parent PLUS loans that parents took out on their behalf

INvestED offers student loan refinancing to Indiana residents and students who attended school in Indiana. They offer a variety of repayment options, competitive interest rates, and flexible terms. INvestED is best if you are an Indiana resident or attended school in Indiana and want access to different repayment options.

Best Features

Drawbacks

• Competitive interest rates • You can refinance without a degree • Offers up to 36 months of academic deferment

• Only available to students that are residents of or attended school in Indiana • No biweekly payment via autopay • You can’t refinance parent PLUS loans in your name • Cosigner release option after 48 months of timely payments

ISL Education Lending is a nonprofit student lender offering both private student loans and student loan refinancing. ISL Education Lending is best for borrowers who want to work with a nonprofit lender, want competitive interest rates, or want to refinance without having a degree.

Best Features

Drawbacks

• Competitive interest rates and zero fees • You can refinance without a degree • Cosigner release option after 24 months

• Only one loan repayment term for in-school refinancing • Students cannot take over parent PLUS loans that parents took out on their behalf • No biweekly payment via autopay

LendKey’s student loan refinancing is a good option if you have graduated, have a strong credit score, and have stable income. A great feature of LendKey is that they will connect you with a network of 100+ lesser known credit unions and community banks so you can work with and take out loans from smaller institutions. LendKey is best if you are a creditworthy borrower and want to work with smaller lenders with low rates and good customer service.

Best Features

Drawbacks

• Work with a credit union or community bank, rather than a traditional lender • Access to competitive interest rates • Offers up to 18 months of forbearance • Free borrower benefits like Career Assistance, Credit Health Analysis, and Federal Student Loan Assistance

• Eligibility criteria excludes part-time students, parents, and non-U.S. citizens/permanent residents • Varying cosigner release policies • Loans aren’t available in Maine, Nevada, North Dakota, Rhode Island, or West Virginia • Biweekly payment via autopay is not available • You may have to become a member of a credit union

Nelnet Bank offers student loan refinancing for both private and federal student loans, including parent PLUS loans. Nelnet Bank also offers a flexible forbearance policy and competitive interest rates. Nelnet Bank is best if you are looking for competitive rates and want the ability to refinance student loans, including parent PLUS loans.

Best Features

Drawbacks

• Competitive interest rates • You can refinance parent PLUS loans in your name • Offers 12 months of forbearance due to economic hardship or natural disaster • Cosigner release option after 24 months of timely payments • Flexible repayment options

• Strict eligibility criteria • No biweekly payment via autopay • Not accessible to international students or borrowers with student visas

SoFi is one of the biggest student loan refinancing companies in the industry. You have to have an associate’s degree or higher to qualify, but if you do qualify, you’ll have access to a wide variety of repayment options and exclusive member benefits. SoFi is best if you have at least an associate’s degree, are a creditworthy borrower, and want to take advantage of their benefits.

Best Features

Drawbacks

• Competitive interest rates • Students can refinance parent PLUS loans in their own name • Comes with borrower protections (forbearance and deferment)

• Unclear about credit requirements • No cosigner release • Refinancing is unavailable to borrowers without a degree • No spousal consolidation loans

Final Thoughts from the Nest

While there are a variety of factors that make a lender or refinance loan good, the best loan will always be the one that works best for you. To discover the best refinancing companies and which option is best for you, complete the Sparrow application.

In just a few minutes, we’ll show you what refinance loans you qualify for with 15+ top lenders. Then, we’ll help guide you through the process of selecting the best refinance loan so you can be confident in your lending decision.

Sparrow’s goal is to give you the tools and confidence you need to improve your finances. Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. While we make an effort to include the best deals available to the general public, we make no warranty that such information represents all available products.

LendKey offers both private student loans and student loan refinancing. By connecting borrowers with a network of 100+ lesser-known credit unions and community banks, LendKey allows you to work with smaller lenders with low rates and good customer service, rather than traditional lending institutions. LendKey’s student loan refinance offering is available to graduates with strong credit and stable income. It’s best if you want to work with a credit union or community bank to access loan offers you otherwise might have overlooked.

Fixed APR Range: 7.11% to 11.18%

Variable APR Range: N/A

Loan Amounts: $5,000 to $300,000, depending on degree

• Work with a credit union or community bank, rather than a traditional lender • Access to competitive interest rates • Offers up to 18 months of forbearance • Free borrower benefits like Career Assistance, Credit Health Analysis, and Federal Student Loan Assistance

• Eligibility criteria excludes part-time students, parents, and non-U.S. citizens/permanent residents • Varying cosigner release policies • Loans aren’t available in Maine, Nevada, North Dakota, Rhode Island, or West Virginia • Biweekly payment via autopay is not available • You may have to become a member of a credit union

Compare LendKey Rates:

Rather than searching for lenders one-by-one, we recommend starting the process with an automated student loan search tool. With the free Sparrow application, you can see the rates and terms you’d qualify for with 17+ premier lenders.

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

LendKey allows you to access refinance offers from a network of non-traditional lenders that you otherwise might have overlooked. On its platform, LendKey connects you with hundreds of community banks and credit unions simultaneously. While the credit unions and community banks don’t have the name recognition that some of the traditional banks and online lenders have, they typically offer lower rates and personalized customer service. In addition, the credit unions and community banks are often non-profits, so you’ll be working with a lender that has your best interest in mind.

Competitive interest rates and zero fees for qualified borrowers

When looking to refinance your student loan, finding a low interest rate is typically a top priority. If you qualify for a LendKey student loan refinance, you’ll have access to competitive interest rates from credit unions and community banks that you might not be able to find elsewhere. While most of the lenders on LendKey’s platform do not charge any origination fees, application fees, or prepayment penalties, some may charge late fees or insufficient funds fees. The terms will vary depending on which lender you choose, so be sure to read the terms and conditions of your loan carefully.

LendKey Student Loan Refinance

Fixed APR*

7.11% to 11.18%

Variable APR*

N/A

*Rates as of September 14, 2023. May include 0.25% AutoPay Discount, which requires you to agree to make your scheduled monthly payments by an automatic monthly deduction (ACH) from a savings or checking account.

Offers up to 18 months of forbearance due to economic hardship or natural disaster

If you experience economic hardship or a natural disaster, LendKey offers generous forbearance options (a pause on your repayment due to financial hardship, unemployment, or a disability).

On 5, 7, and 10-year loans, LendKey allows you to postpone payments for up to four months at a time, for up to 12 months total.

On 15 and 20-year loans, LendKey offers up to 18 months of forbearance, in six-month increments. While LendKey handles forbearance on a case-by-case basis, it can be a helpful safety net if you were to fall into financial hardship.

Free borrower benefits like Career Assistance, Credit Health Analysis, and Federal Student Loan Assistance

When you borrow through LendKey’s platform, you’ll get free access to special borrower benefits that help you achieve your financial and personal goals. These benefits include:

Career Assistance: LendKey partners with NextJob to offer free tools and online resources to help you succeed, including:

Online mock interviews

A resume builder

Hidden job opportunities waiting to be uncovered

A personality test to help you find the right career path

Credit Health Analysis: To help you reach your financial goals, LendKey has partnered with Curu, a platform that provides comprehensive credit analysis designed to help you improve your credit health

Curu analyzes your spending, net worth, and credit utilization to generate personalized tasks that show your path to credit success.

Curu displays your real-time financial account information all in one place so you always know where you stand.

Curu sends you notifications for upcoming credit card payment due dates so you’ll never miss a payment again.

Federal Student Loan Assistance: LendKey partners with Savi to provide an online, concierge service that searches across 150+ federal loan forgiveness and repayment options and recommends a path forward based on a borrower’s unique financial situation and goals. Savi then automates and digitizes the application process to reduce mistakes, simplify the process, and save time.

Access a free, instant estimate of monthly savings

Detect eligibility & simplify enrollment for national and state repayment and forgiveness programs

Receive 1:1 support as needed from a team of student loan experts

Drawbacks: LendKey Student Loan Refinance

Strict eligibility criteria

In order to qualify for student loan refinance through LendKey, borrowers must meet the following criteria:

A U.S. citizen or permanent resident

Graduated with at least an associate degree

You or your cosigner have a credit score of 660

You have an annual income of $24,000 per year, or $12,000 per year with a cosigner

LendKey’s strict eligibility criteria excludes non-U.S. citizens/permanent residents, non-graduates, parents, and those who don’t meet the credit or income requirements.

Haven’t earned an associate’s degree?EDvestinU accepts borrowers without a degree.

Don’t have a credit score of 660 (or a creditworthy cosigner)? Earnest accepts borrowers with a lower credit score.

If you do not meet LendKey’s criteria for a student loan, you may want to look elsewhere to refinance your private student loan. To check your rates across multiple lenders at once, try using Sparrow’s free search engine. In just two minutes, you can receive real, personalized offers from over 15 different lenders all bidding for your business. And best of all, it won’t impact your credit score.

Varying cosigner release policies

Most private student lenders require or strongly encourage you to apply with a cosigner. Given that young people generally have no/limited credit history, a cosigner can help you qualify for better loan terms.

If you earn less than $24,000 per year or have fewer than 36 months of credit history, a cosigner is required in order to borrow from LendKey.

Unfortunately, it’s not clear how quickly you can release your cosigner from your LendKey loan. Since LendKey partners with credit unions and community banks (each of which have their own internal policies), you will need to check with your specific lender to confirm their cosigner release policy.

Loans aren’t available in certain states

LendKey does not offer student loan refinance to borrowers who live in Maine, Nevada, North Dakota, Rhode Island, or West Virginia. If you live in any of these states, try using our rate comparison tool to see which refinance lenders you qualify with.

No biweekly payment via autopay

When you repay your student loan, your payments are due monthly by default. Instead, some borrowers choose to make biweekly payments via autopay — where you automatically pay half your monthly amount once every two weeks. Many borrowers use biweekly autopay in an effort to pay off their student debt faster and pay less in interest over the lifetime of the loan.

Unfortunately, when you borrow through LendKey, you don’t have the option to make biweekly payments via autopay.

You do, however, have the option to make greater-than-minimum payments via autopay. This means you have the option to pay more than your monthly balance in order to reduce the interest that accrues over time. With LendKey, you can set this up automatically so that the desired monthly payment is drawn from your bank account at the end of each month.

You may have to become a member of a credit union

One of the major advantages of borrowing through LendKey is that the platform allows you to access loan offers from a network of non-traditional lenders (credit unions and community banks) that you otherwise might have overlooked.

Unfortunately, that also means you may have to become a member of the institution you borrow from, which typically costs around $5. Although the process of becoming a member of a credit union is relatively simple, it adds another step to the borrowing process that traditional banks and online lenders don’t require.

LendKey Student Loan: The Nuts and Bolts

Interest Rates, Fees, and Terms

Fixed APR Range

7.11% to 11.18%

Variable APR Range

N/A

Loan Terms

5, 7, 10, 15, or 20 years.

Loan Amounts

$5,000 to $125,000 for undergraduate degrees; up to $250,000 for graduate degrees; and up to $300,000 for medical, dental or veterinary degrees.

Ability to transfer a parent loan to the student

No.

Application or Origination Fee

No.

Prepayment Penalty

No.

Late Fees

Yes (If payment is not made within 15 days of the due date, the late fee is $5 to $10, depending on the lender).

Eligibility Requirements – Financial

Minimum Credit Score

660.

Minimum Income

24,000 per year, $12,000 per year with a cosigner.

Typical Credit Score of Approved Borrowers or Cosigners

751.

Typical Income of Approved Borrower

$65,000.

Maximum Debt-to-Income Ratio

50%.

Ability to qualify if you’ve filed for bankruptcy

Yes, after five years.

Eligibility Requirements – Personal

Citizenship

Borrowers must be U.S. citizens or permanent residents.

Location

Available to borrowers in all 50 states, except Maine, Nevada, North Dakota, Rhode Island, and West Virginia.

Must have graduated

Yes, with at least an associate degree.

Must have attended a school authorized to receive federal aid

Yes.

Percentage of borrowers who have a cosigner

37%+.

Repayment Options

Academic Deferment

No.

Military Deferment

No.

Disability Deferment

Did not disclose.

Forbearance

On 5, 7, and 10-year loans, postpone payments for up to four months at a time, for up to 12 months total. On 15 and 20-year loans, postpone payments for up to six months at a time, for 18 months total.

Cosigner Release

Did not disclose.

Death or Disability Discharge

Not guaranteed by the loan agreement, but common practice, according to LendKey.

Loan discharge if cosigner dies or becomes disabled

No.

Autopay

Allows for surplus payments via autopay: Yes. Allows for biweekly payments via autopay: No.

Customer Service

Loan Servicer

LendKey.

In-house Customer Service Team

Yes.

Process for Escalating Concerns

No.

Borrowers get assigned a personal customer service representative

No.

Average time from approval to payoff

Did not disclose.

Before you take out a loan from LendKey…

Complete the Sparrow application to compare real rates from more than 15 different lenders to make sure you’re getting the best rate possible.

See real rates, not rate ranges or estimates: Sparrow’s rates mimic those of our lenders so you know what rate you’re getting from each lender.

No impact on your credit score: Checking your rates on Sparrow won’t impact your credit score.

Data Privacy: Sparrow doesn’t sell your information, so don’t worry about getting calls from that random number that won’t leave you alone.

FAQ

Is LendKey a legitimate lender?

Yes, LendKey is legitimate. The platform connects borrowers with credit unions and community banks offering private student loans to undergraduates, graduate students, and parents, as well as student loan refinancing. Since its founding in 2009, LendKey has helped fund $3.1 billion in loans for 99,000-plus borrowers — it also services more than $2 billion worth of student loans.

Is LendKey available in all 50 states?

LendKey is available to borrowers in all 50 states, except Maine, Nevada, North Dakota, Rhode Island, and West Virginia.

How long does it take to get a LendKey student loan?

Submitting an application through LendKey takes a few minutes. Once you’ve submitted your loan application, LendKey will instantaneously return a decision about your eligibility. If you qualify, you will receive the rate and terms of your loan.

It may take some time to actually receive your loan. However, you can speed up the process by requesting debt payoff letters from your current lenders and loan servicers.

What happens if I don’t qualify for a LendKey student loan?

If you don’t qualify for LendKey student loan refinance, the company will inform you why. Depending on the reason, you may consider applying with a qualified cosigner or try with a different lender. To check your rates across multiple lenders at once, try using Sparrow’s free search engine. In just two minutes, you can receive real, personalized offers from over 15 different lenders all bidding for your business. Best of all, it won’t impact your credit score.

Are LendKey student loans federal or private?

LendKey’s student loans are private. Before you take out a private student loan, we recommend that you exhaust your federal funding options, including grants and scholarships.

Does applying for a loan through LendKey hurt my credit score?

In order to estimate what rate you qualify for, LendKey conducts a soft credit check — this does not affect your credit score. If you choose to accept the LendKey refinance offer, the company will conduct a hard credit check to verify your information. A hard credit check may temporarily impact your credit score.

EdvestinU is a student loan program from the nonprofit New Hampshire Higher Education Loan Corp. They offer private student loans and student loan refinancing to students across the country. In order to qualify for EdvestinU’s student loan refinancing, you do not need to be from New Hampshire or even have graduated school. EdvestinU’s refinance offering is best for those who do not have a degree and are looking to refinance up to $200,000 of student loans.

• Work with a non-profit, rather than a traditional lender • You can refinance your students loans without a degree • Exclusive benefits for New Hampshire residents

• Maximum loan of $200,000 is lower than most refinance lenders • Students cannot take over parent PLUS loans that parents took out on their behalf

Compare EdvestinU Refinance Rates:

Rather than searching for lenders one-by-one, we recommend starting the process with an automated student loan search tool. With the free Sparrow application, you can see the rates and terms you’d qualify for with 17+ premier lenders.

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

Work with a non-profit, rather than a traditional lender

EdvestinU has been helping families across the country finance the cost of their college education for nearly 60 years. EdvestinU is not affiliated with any school. As a non-profit, its goal is to save you money by offering the most competitive rates possible. While EdvestinU doesn’t have the name recognition that some of the traditional banks and online lenders have, it offers low rates and personalized customer service.

You can refinance your student loan without a degree

While most lenders require you to have graduated in order to refinance your student loan, EdvestinU accepts borrowers who don’t have a degree. This is a huge benefit to borrowers who left school before earning their degree.

Regardless of whether or not you have earned your degree, you will still need to meet EdvestinU’s credit and income requirements to qualify for refinancing.

Credit Score: You’ll need a credit score of at least 700.

Income: You’ll need $30,000 in gross income if you plan to refinance less than $100,000. You’ll need $50,000 in gross income if you plan to refinance more than $100,000.

If you do not meet that criteria, you could still be eligible for refinancing if you apply with a cosigner who does.

Exclusive benefits for New Hampshire residents

EdvestinU, as well as many other private student lenders, offers a 0.25% discount if you enable automatic payments. This is the lender’s way of incentivizing you to turn on autopay so that you don’t miss a payment.

EdvestinU has taken this to another level by offering New Hampshire residents a 1% rate reduction on fixed rate loans and a 0.25% rate reduction on variable loans.

EdvestinU also offers in-person support and counseling to borrowers from New Hampshire.

If you’re a New Hampshire resident, EdvestinU might be the best option for you.

Drawbacks of Refinancing with EdvestinU

Maximum loan of $200,000 is lower than most lenders

While other lenders often will refinance loans up to the total cost of attendance, the maximum loan amount that EdvestinU will refinance is $200,000. Accordingly, EdvestinU is a great option if you are refinancing relatively smaller student loans. However, if you are refinancing loans from medical school or graduate school that exceed $200,000, you might want to consider other lenders that accept larger loans.

Students cannot take over parent PLUS loans that parents took out on their behalf

If your parent has taken out a Parent PLUS loan or a private student loan in their name, some lenders give your parent the option to transfer the loan to your name (so long as you are the primary applicant). However, EdvestinU does not allow students to refinance parent PLUS loans in the student’s name.

If you are a parent who took out a parent PLUS loan, you can still refinance that loan through EdvestinU — it will just be in your name, not the student’s name.

If you’re looking for a lender that does allow you to transfer parent PLUS loans to the student, you may want to consider SoFi.

EdvestinU: The Nuts and Bolts

Interest Rates, Fees, and Terms

Fixed APR Range

4.41% to 7.78%

Variable APR Range

8.04% to 9.79%

Loan Terms

5, 10, 15 or 20 years.

Loan Amounts

$7,500 to $200,000.

Ability to transfer a parent loan to the student

No.

Application or Origination Fee

No.

Prepayment Penalty

No.

Late Fees

Yes, five percent of the monthly payment.

Eligibility Requirements – Financial

Minimum Credit Score

700.

Minimum Income

$30,000 if you plan to refinance less than $100,000; if you plan to refinance more than that, the minimum income is $50,000.

Typical Credit Score of Approved Borrowers or Cosigners

756.

Typical Income of Approved Borrower

Approximately $70,000.

Maximum Debt-to-Income Ratio

43%.

Ability to qualify if you’ve filed for bankruptcy

Yes, after 10 years have passed.

Eligibility Requirements – Personal

Citizenship

Must be a U.S. citizen or a permanent resident.

Location

Available to borrowers in all 50 states.

Must have graduated

No.

Must have attended a school authorized to receive federal aid

Yes.

Percentage of borrowers who have a cosigner

52%.

Repayment Options

Academic Deferment

Yes, but interest-only payments are due during the deferment.

Military Deferment

Yes, but interest-only payments are due during the deferment.

Disability Deferment

Yes, you can postpone payment while undergoing rehab for a disability.

Economic Hardship Deferment

Yes, borrowers are eligible for 12 months of economic hardship deferment, in three-month increments, over the life of the loan.

Forbearance

Discretionary forbearance is available for 12 months.

Cosigner Release

Yes, after 36 months of consecutive, on-time payments. Borrowers must also have a credit score greater than 749 and a minimum gross income of $30,000.

Death or Disability Discharge

The loan will be forgiven if the borrower dies, but not in instances of total or permanent disability.

Loan discharge if cosigner dies or becomes disabled

No.

Autopay

Allows for surplus payments via autopay: Yes. Allows for biweekly payments via autopay: No.

Customer Service

Loan Servicer

Firstmark Services

In-house Customer Service Team

Yes.

Process for Escalating Concerns

Yes.

Borrowers get assigned a personal customer service representative

No.

Average time from approval to payoff

At least 30 days.

Before you take out a loan from EdvestinU…

Complete the Sparrow application to compare real rates from more than 15 different lenders to make sure you’re getting the best rate possible.

See real rates, not rate ranges or estimates: Sparrow’s rates mimic those of our lenders so you know what rate you’re getting from each lender.

No impact on your credit score: Checking your rates on Sparrow won’t impact your credit score.

Data Privacy: Sparrow doesn’t sell your information, so don’t worry about getting calls from that random number that won’t leave you alone.

FAQ

Is EdvestinU a legitimate lender?

Yes, EdvestinU is a legitimate lender that has close to sixty years of experience lending and refinancing in higher education.

Is EdvestinU available in all 50 states?

Yes, EdvestinU is available in all 50 states.

How long does it take to get an EdvestinU student loan?

Submitting an application through EdvestinU takes a few minutes. Once you’ve submitted your loan application, EdvestinU will immediately return a decision about your eligibility. If you qualify, you will receive the rate and terms of your loan.

It may take some time to actually receive your loan. However, you can speed up the process by requesting debt payoff letters from your current lenders and loan servicers.

What happens if I don’t qualify for an EdvestinU student loan?

If you don’t qualify for an EdvestinU student loan, the company will inform you why. Depending on the reason, you may consider applying with a qualified cosigner or trying with a different lender. To check your rates across multiple lenders at once, try using Sparrow’s free search engine. In just two minutes, you can receive real, personalized offers from over 15 different lenders ready to help you. And best of all, it won’t impact your credit score.

Are EdvestinU student loans federal or private?

EdvestinU loans are private loans. Before you take out a private student loan, we recommend that you exhaust your federal funding options, including grants and scholarships.

Does applying for a loan through EdvestinU hurt my credit score?

In order to estimate what rate you qualify for, EdvestinU conducts a soft credit check — this does not affect your credit score. If you choose to accept the EdvestinU loan, the company will conduct a hard credit check to verify your information. A hard credit check may temporarily impact your credit score.

Refinancing your student loans can save you thousands over the life of your loan. By refinancing, you can swap your current student loan(s) for a new loan with a better interest rate or terms.

If you have excellent credit or stable income, or a cosigner who does, you may benefit from refinancing your student debt. To begin the process of refinancing, explore the best student loan refinancing options from our lending partners below.

Compare Student Loan Refinancing Rates

Finding the right refinancing option should be a simple. Use Sparrow to find the best student loan refinance optionfor you. Sparrow shows you the most important information and simplifies the entire process.

The Arkansas Student Loan Authority offers student loan refinancing to Arkansas residents or students who have attended a school in the state. They offer competitive rates and flexible terms to those who qualify. ASLA is best if you either live in or attended school in Arkansas and want competitive interest rates and flexible loan terms.

Best Features

Drawbacks

• Competitive interest rates • Ability to refinance several types of loans • Variety of repayment options • Cosigner release option after 48 months • Offers 0.25% interest rate reduction for opting into auto-debit payments

• Strict residency requirements • Inaccessible for international students

Brazos is a nonprofit lender that provides student loan refinancing to Texas residents. While you do need to have at least an undergraduate degree to refinance with Brazos, you will receive competitive interest rates and flexible terms if you qualify. Brazos is best if you are a Texas resident and have at least an undergraduate degree, though the degree does not have to be from a Texas school.

Best Features

Drawbacks

• Work with a nonprofit, rather than a traditional lender • Competitive interest rates • Variety of repayment terms ranging from 5 to 20 years • Generous forbearance options

• Strict eligibility criteria • No cosigner release • No bi-weekly payment via autopay • Students cannot take over parent PLUS loans that parents took out on their behalf

College Ave offers student loan refinancing and is known for their strong customer service, competitive interest rates, and flexible loan terms. For example, College Ave offers 6- or 9-year loans, which is unlike many other private lenders. College Ave is best if you want access to good customer service and a flexible repayment term that better matches your budget.

Best Features

Drawbacks

• Strong customer experience • Competitive rates • Choose any loan term between 5 and 15 years including nonstandard terms such as 6 or 9 years

• Limited eligibility criteria • Unclear forbearance policy • Not available to borrowers without a degree, visa holders, or those with parent PLUS loans • Doesn’t allow spousal consolidation loans

Earnest offers student loan refinancing with customizable repayment plans, allowing you to choose your repayment term down to the month. Earnest also has forward-looking eligibility requirements and offers competitive interest rates. Earnest is best if you don’t have a cosigner and want a repayment plan customized to your situation.

Best Features

Drawbacks

• Competitive interest rates • Customizable payments and loan terms • Option to skip one monthly payment every year • Allows biweekly payments via autopay

• Refinancing is unavailable in Kentucky and Nevada • Variable interest rates aren’t available for borrowers in all states • You can’t apply with a cosigner • Student borrowers cannot take over parent PLUS loans that parents took out on their behalf

INvestED offers student loan refinancing to Indiana residents and students who attended school in Indiana. They offer a variety of repayment options, competitive interest rates, and flexible terms. INvestED is best if you live in Indiana or attended school in Indiana and want access to different repayment options.

Best Features

Drawbacks

• Competitive interest rates • You can refinance without a degree • Offers up to 36 months of academic deferment

• Only available to students that are residents of or attended school in Indiana • No biweekly payment via autopay • You can’t refinance parent PLUS loans in your name • Cosigner release option after 48 months of timely payments

ISL Education Lending is a nonprofit student lender offering both private student loans and student loan refinancing. ISL Education Lending is best if you want to work with a nonprofit lender, want competitive interest rates, or want to refinance without having a degree.

Best Features

Drawbacks

• Competitive interest rates and zero fees • You can refinance without a degree • Cosigner release option after 24 months

• Only one loan repayment term for in-school refinancing • Students cannot take over parent PLUS loans that parents took out on their behalf • No biweekly payment via autopay

LendKey’s student loan refinancing is a good option if you have graduated, have a strong credit score, and have stable income. A great feature of LendKey is that they will connect you with a network of 100+ lesser known credit unions and community banks so you can work with and take out loans from smaller institutions. LendKey is best if you are a creditworthy borrower and want to work with smaller lenders with low rates and good customer service.

Best Features

Drawbacks

• Work with a credit union or community bank, rather than a traditional lender • Access to competitive interest rates • Offers up to 18 months of forbearance • Free borrower benefits like Career Assistance, Credit Health Analysis, and Federal Student Loan Assistance

• Eligibility criteria excludes part-time students, parents, and non-U.S. citizens/permanent residents • Varying cosigner release policies • Loans aren’t available in Maine, Nevada, North Dakota, Rhode Island, or West Virginia • Biweekly payment via autopay is not available • You may have to become a member of a credit union

Nelnet Bank offers student loan refinancing for both private and federal student loans, including Parent PLUS loans. Nelnet Bank also offers a flexible forbearance policy and competitive interest rates. Nelnet Bank is best if you are looking for competitive rates and want the ability to refinance Parent PLUS loans.

Best Features

Drawbacks

• Competitive interest rates • You can refinance parent PLUS loans in your name • Offers 12 months of forbearance due to economic hardship or natural disaster • Cosigner release option after 24 months of timely payments • Flexible repayment options

• Strict eligibility criteria • No biweekly payment via autopay • Not accessible to international students or borrowers with student visas

SoFi is one of the biggest student loan refinancing companies in the industry. You have to have an associate’s degree or higher to qualify, but if you do qualify, you’ll have access to a wide variety of repayment options and exclusive member benefits. SoFi is best if you have at least an associate’s degree, are a creditworthy borrower, and want to take advantage of their borrower benefits.

Best Features

Drawbacks

• Competitive interest rates • Students can refinance parent PLUS loans in their own name • Comes with borrower protections (forbearance and deferment)

• Unclear about credit requirements • No cosigner release • Refinancing is unavailable to borrowers without a degree • No spousal consolidation loans

Frequently Asked Questions About Student Loan Refinancing

Can I refinance just my private student loans?

Yes. You can refinance just your private student loans.

Is it a good time to refinance private student loans?

Yes. You can refinance private student loans at any time. If you have federal student loans, however, we recommend waiting until the federal student loan forbearance is over.

Can you refinance a private student loan into a federal one?

No. Because private student loans are provided by private financial institutions, you cannot transfer them to federal student lenders. However, you can refinance a federal student loan into a private student loan.

What is a good interest rate for student loan refinancing?

The goal of student loan refinancing is to secure a lower interest rate or better terms than what you currently have. So, any interest rate lower than what you currently have would be a good interest rate.

Sparrow’s goal is to give you the tools and confidence you need to improve your finances. Many or all of the products shown here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. While we make an effort to include the best deals available to the general public, we make no warranty that such information represents all available products.

According to Forbes, the median total cost of becoming a doctor in 2020 was between $255,517 to $337,584, leaving many with hefty student debt totals.

If you’re looking to lower the costs of your medical school loans, consider loan refinancing. Refinancing is the process of taking out a new loan with better terms to repay your current debt. By scoring a lower interest rate or monthly payment, you may be able to alleviate some of the financial burden your medical school loans are causing you.

Keep reading for the complete guide on how, when, and where to refinance medical school loans.

When Can You Refinance Medical School Loans?

You can refinance medical school loans during residency or early in your career as an attending physician. However, the timeline of when you can refinance ultimately depends on your lender.

While refinancing as early as possible will be the most advantageous thing to do, the most important thing is that you refinance when you are in the financial standing to do so.

If you can get more competitive terms by refinancing during residency but it puts you in a tough financial spot, it may not be the optimal thing to do. It’s better to hold off on refinancing if doing so would cause you to miss a payment or wind up in loan default.

Who Should Refinance Medical School Loans?

You should refinance your medical school loans if:

You borrowed private student loans.

You are not/will not use your federal loan benefits.

You have better, improved credit from when you first borrowed your loans.

If you are a federal borrower, keep in mind that refinancing will convert your loans from federal to private loans. This means you will lose any federal benefits you have, such as an income-driven repayment plan, potential loan forgiveness, or flexible loan deferment/forbearance.

The Process of Refinancing

If you decide you want to refinance your medical school loans, you’ll want to take the following steps.

Determine If It Makes Sense for You

First and foremost, you should only refinance medical school loans if it will benefit you.

If you have federal loans, note that you will lose your federal benefits if you decide to refinance. If you don’t plan to use them, refinancing your loans for a better interest rate or monthly payment may outweigh any federal benefits you have.

If you have private loans, consider your current financial standing. If you have a better credit score from when you last applied and can qualify for better loan terms, refinancing may be the way to go. If you do not qualify for better loan terms, there may be no point in refinancing.

Compare Prequalification Offers

To be sure refinancing makes sense for you, see what you qualify forbefore submitting a formal loan refinance application with a lender. You can do this by completing Sparrow’s free, 3-minute prequalification application.

We’ll show you what loan refinancing options you qualify for across 15+ private lenders — without damaging your credit score.

Submit a Formal Loan Application

After determining which lender you’d like to refinance with, submit your formal loan application.

You’ll want to gather the following information for a speedy application process:

Your Social Security Number

Optional: Your cosigner’s Social Security Number (You do not need this information if you are not borrowing with a cosigner.)

Tax Information

Tax Returns

IRS W-2

Optional: Cosigner’s tax information (Again, you do not need this information if you are not borrowing with a cosigner.)

Personal Income Information

Information on any financial assets you have, including:

Cash in your checking and/or savings account

Investments (stocks, bonds, etc.)

Business assets

Mortgages

Start Making Loan Payments After Your New Loan Is Approved

Once your new loan is approved and you’ve signed your promissory note, your new lender will pay off your old lender. Then, you can start making loan payments on your new loan as outlined in your loan contract.

If you’re an Arkansas resident looking to refinance your medical loans, consider the Arkansas Student Loan Authority. ASLA is a state entity that offers loan refinancing for Arkansas residents.

Fixed APR range: 3.50% to 7.48% Variable APR range: N/A Refinancing amount: $5,000 to $250,000

Brazos is a non-profit lender that offers competitive loan refinancing terms for Texas residents. To qualify with Brazos, it is recommended that you have a strong credit score, a steady income, and at least a bachelor’s degree.

Fixed APR range: 4.90% to 6.99% Variable APR range: 5.32% to 9.12% Refinancing amount: $10,000 to $400,000

College Ave is a non-profit that offers competitive interest rates, zero fees, and a cosigner release option for qualifying borrowers. A highlight about College Ave is that they do not require borrowers to have a degree or qualify for financial aid. So, if you did not complete your medical degree but still have your loans, College Ave will be a great option for you.

Fixed APR range: 6.99% to 11.99% Variable APR range: 6.99% to 11.99% Refinancing amount: $5,000 to $300,000, depending on degree type

Refinancing with Earnest gives you access to merit-based rates, customizable payment, and loan terms, as well as the option to skip one monthly payment every year.

Fixed APR range: 4.96% to 9.79% (including 0.25% auto-pay discount) Variable APR range: 5.49 % to 9.74% (including 0.25% auto-pay discount) Refinancing amount: $5,000 ($10,000 for California residents) to $500,000

EdvestinU is a student loan program under the New Hampshire Higher Education Loan Corp, a non-profit based in New Hampshire. You can refinance your student loans with EdvestinU without a degree and have access to special perks if you are a New Hampshire resident. You must be a U.S. citizen or permanent resident who qualifies for financial aid.

Fixed APR range: 4.41% to 7.78% Variable APR range: 8.04% to 9.79% Refinancing amount: $7,500 to $200,000

INvestED is best for students who are Indiana residents or attend school in Indiana. You must be a U.S. citizen or qualifying resident who receives financial aid at your academic institution. The lender offers competitive interest rates, 36 months of academic deferment, and does not require a degree to qualify.

Fixed APR range: 5.85% to 9.48% Variable APR range: 8.63% to 12.27% Refinancing amount: $5,000 to $250,000

ISL Education Lending is a non-profit that offers loan refinancing options with competitive interest rates, zero fees, and a cosigner release option. You also do not need a degree to qualify, which is a perk.

You must be a U.S. citizen or permanent resident who is not based in Maine or Oregon to qualify.

Fixed APR range: 3.94% to 8.48% Variable APR range: N/A Refinancing amount: $5,000 ($10,000 for California residents) to $300,000

LendKey connects borrowers with small lenders, credit unions, and community banks. You can refinance with LendKey if you’re a graduate student with a steady income and strong credit history.

Fixed APR range: 7.11% to 11.18% Variable APR range: N/A Refinancing amount: $5,000 to $300,000 (depending on degree type)

MPOWER is a great lender that refinances loans for domestic, international, and DACA undergraduate and graduate students. To refinance with MPOWER, your loan(s) must not be cosigned.

Nelnet Bank offers competitive terms, including flexible repayment options, a cosigner release option, 12 months of forbearance, and the ability to refinance your parent PLUS loan in your name.

To refinance your student loans with Nelnet Bank, you must be a U.S. citizen or a permanent resident with a Social Security Number. You also must have obtained at least a bachelor’s degree.

Fixed APR range: 7.12% to 11.19% Variable APR range: 7.60% to 14.50% Refinancing amount: $5,000 to $225,000

SoFi is a well-established name in the student loan industry that offers one of the most competitive rates for loan refinancing. To qualify, you must have an associate’s degree or higher.

SoFi also allows borrowers to refinance parent PLUS loans in their own name, offers loan forbearance and deferment, and doesn’t have any origination fees.

Fixed APR range: 4.49% to 8.99% Variable APR range: 4.49% to 8.99% Refinancing amount: $5,000 to your total outstanding balance

Refinancing medical school loans is a great way to save money in the long run. Like all things, doing your due diligence is crucial. Look into all of your refinancing options so you know you are getting the best offer on the market.

Student loan refinancing is one of the best ways to save money when paying off your student loans. By refinancing, you’d take out a new loan with more favorable terms to repay your current debt. Ideally, this new loan will have a lower interest rate or monthly payment (or both). Although you may be wondering what credit score is needed to refinance your student loan.

Unfortunately, not everyone is eligible. Oftentimes, you need a strong credit score to refinance student loans, along with other qualifications to prove that you are a creditworthy borrower. Here’s what you need to know.

Do You Need Good Credit to Refinance Student Loans?

Yes, student loan lenders will generally require borrowers to have good credit to qualify for loan refinancing. This usually means a credit score of 700 or higher.

Good credit not only determines whether you are eligible for loan refinancing, but can influence how competitive your interest rate is. Certain lenders will refinance student loans for borrowers with weak credit, but the interest rates on these loans are usually higher.

If you want to refinance your loans, it’s crucial to look across multiple lenders to make sure you’re getting the most competitive terms.

If you’re an Arkansas resident looking to refinance your medical loans, consider the Arkansas Student Loan Authority. ASLA is a state entity that offers loan refinancing for Arkansas residents.

Fixed APR range: 3.50% to 7.48% Variable APR range: N/A Refinancing amount: $5,000 to $250,000

Brazos is a non-profit lender that offers competitive loan refinancing terms for Texas residents. To qualify with Brazos, it is recommended that you have a strong credit score, a steady income, and at least a bachelor’s degree.

Fixed APR range: 4.90% to 6.99% Variable APR range: 5.32% to 9.12% Refinancing amount: $10,000 to $400,000

College Ave offers competitive interest rates, zero fees, on-site loan servicing, and a cosigner release option for qualifying borrowers. A highlight about College Ave is that they do not require borrowers to have a degree or qualify for financial aid.

You must be a U.S. citizen or a permanent resident who is not based in Maine or Oregon to qualify for loan refinancing with College Ave.

Fixed APR range:6.99% to 11.99% Variable APR range:6.99% to 11.99% Refinancing amount: $5,000 to $300,000, depending on degree type

Earnest is well-known in the student loan industry and is backed by competitive refinancing terms and student loans. By refinancing your student loans with Earnest, you have access to merit-based rates, customizable payments and loan terms, as well as the option to skip one monthly payment every year.

Refinancing is not available in Kentucky and Nevada, and you will not have the option to add a cosigner to your application.

Fixed APR range:4.96% to 9.79% (including 0.25% auto-pay discount) Variable APR range:5.49% to 7.94% (including 0.25% auto-pay discount) Refinancing amount: $5,000 ($10,000 for California residents) to $500,000

EdvestinU is a student loan program under the New Hampshire Higher Education Loan Corp, a non-profit based in New Hampshire. You can refinance your student loans with EdvestinU without a degree and have access to special perks if you are a New Hampshire resident. You must be a U.S. citizen or permanent resident who qualifies for financial aid.

Fixed APR range: 4.41% to 7.78% Variable APR range:8.04% to 9.79% Refinancing amount: $7,500 to $200,000

INvestED is best for students who are Indiana residents or attend school in Indiana. You must be a U.S. citizen or qualifying resident who receives financial aid at your academic institution. The lender offers competitive interest rates, 36 months of academic deferment, and does not require a degree to qualify.

Fixed APR range: 5.85% to 9.48% Variable APR range: 8.63% to 12.27% Refinancing amount: $5,000 to $250,000

ISL Education Lending is a non-profit that offers loan refinancing options with competitive interest rates, zero fees, and a cosigner release option. You also do not need a degree to qualify, which is a perk.

You must be a U.S. citizen or permanent resident who is not based in Maine or Oregon to qualify.

Fixed APR range: 3.94% to 8.48% Variable APR range: N/A Refinancing amount: $5,000 ($10,000 for California residents) to $300,000

LendKey connects borrowers with small lenders, credit unions, and community banks. You can refinance with LendKey if you’re a graduate student with a steady income and strong credit history.

Fixed APR range: 4.99% to 10.68% Variable APR range: 4.54% to 7.39% Refinancing amount: $5,000 to $300,000 (depending on degree type)

MPOWER is a great lender that refinances loans for domestic, international, and DACA undergraduate and graduate students. To refinance with MPOWER, your loan(s) must not be cosigned.

Nelnet Bank is an online bank that provides loan refinancing for qualifying borrowers. They offer competitive terms, including flexible repayment options, a cosigner release option, 12 months of forbearance, and the ability to refinance your parent PLUS loan in your name.

To refinance your student loans with Nelnet Bank, you must be a U.S. citizen or a permanent resident with a Social Security Number. You also must have at least a bachelor’s degree.

Fixed APR range:7.12% to 11.19% Variable APR range:7.60% to 14.50% Refinancing amount: $5,000 to $225,000

SoFi is a well-established name in the student loan industry that offers one of the most competitive rates for loan refinancing. To qualify, you must have an associate’s degree or higher.

SoFi also allows borrowers to refinance parent PLUS loans in their own name, offers loan forbearance and deferment, and doesn’t have any origination fees.

Fixed APR range: 4.49% to 8.99% Variable APR range: 4.49% to 8.99% Refinancing amount: $5,000 to your total outstanding balance

Eligibility Requirements to Refinance Student Loans

While there is a minimum credit score to refinance student loans for many lenders, your credit score isn’t the only consideration. Here are a few other factors that impact your eligibility:

A Strong Credit History

A strong credit history generally consists of the following:

On-time and in-full loan payments

No history of default

No history of bankruptcy

No history of delinquency

Your credit history shows your reliability as a borrower. The stronger your credit history is, the easier it is for you to secure competitive interest rates and loan terms.

Having a steady, consistent income will show lenders that you have a stream of capital you can use to make loan payments.

A Low Debt-to-Income (DTI) Ratio

Your debt-to-Income (DTI) ratio shows the proportion of debt and income that you have. To calculate your DTI, divide your monthly debt payments by your gross monthly income.

For example, let’s say you have $2,000 in monthly payments for outstanding debt and make a monthly income of $5,000. If you divide $2,000 by $5,000, you get .4, which is a DTI of 40%.

If you have a lower DTI, this demonstrates that you make more money than you owe. However, if you have a high DTI, this shows lenders that you owe more than you make. A DTI of 35% or less is considered a good DTI.

Proof of Graduation

Generally, lenders will require borrowers to have a degree to be eligible for loan refinancing. However, there are a few lenders that don’t have this requirement.

What is the Credit Score Requirement to Refinance Student Loans?

It depends. For example, based on the lenders above, the required credit score to refinance student loans varies from 640 to 720. However, the better your score, the better terms you are likely to receive.

What to Do If You Don’t Have the Credit Score to Refinance Your Student Loans?

If you don’t meet the credit requirements to be eligible for student loan refinancing, don’t fret. You may still be able to qualify by adding a cosigner to your application.

A cosigner is an individual who agrees to take responsibility for your loan if you fail to make payments on it. Generally, a cosigner is an immediate family member, relative, or close friend.

Once you identify an individual who is willing to be a cosigner for you, you’ll want to compare the options that allow you to add a cosigner. Look at terms such as interest rate, cosigner release options, repayment terms, and more. Consider using Sparrow as a tool to compare your options and see how different cosigners impact the loan terms.

As you explore your loan refinancing options, remember to compare your options across interest rates, repayment plans, borrower protections, and other important considerations. Loan refinancing is a beneficial thing to do, but you’ll want to find the best option for your personal and financial circumstances.

You don’t have to make this decision alone. Sparrow’s form allows you to find the best student loans with the best interest rates for you. The platform makes it easy for you to compare real pre-qualified rates without having to apply with lenders one-by-one. Save time by finding the ideal interest rate for you with Sparrow!

Sparrow aims to give you the tools and confidence you need to improve your finances. Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. While we make an effort to include the best deals available to the general public, we make no warranty that such information represents all available products.

As a borrower, refinancing your student loans can be beneficial. For example, borrowers who use Sparrow to refinance save, on average, $17,000 over the life of their loan.

That said, the savings can vary greatly depending on the borrower. With that in mind, you might be wondering, “Is refinancing student loans worth it?.”

It’s always a good choice to explore your options to make a financially sound decision for yourself. To determine whether refinancing is worth it for you, here’s what you should know.

How Student Loan Refinancing Works

Loan refinancing is the process of taking out a new loan to pay for your current debt. The new loan should have more favorable terms, such as a lower interest rate or monthly loan payment.

For example, let’s say you currently have a student loan of $80,000 with an 8% interest rate and a 10-year repayment plan. You decide to refinance and qualify for a new loan of $80,000 with a 5% interest rate, with a 15-year repayment plan.

Through refinancing, you have a new loan with a lower interest and longer repayment period.

To refinance your student loans, you need to submit a formal application to the lender of your choice. Generally, lenders are looking for borrowers who have a strong credit history and a low debt-to-income (DTI) ratio.

The Pros and Cons of Refinancing

To better understand if refinancing student loans is worth it for you, consider the pros and cons:

Pros of Refinancing

You Can Have Lower Monthly Payments

If your student loan payments are too high, refinancing can help relieve the financial strain. You can extend your repayment plan to reduce monthly payments and pay the loan over a longer period of time.

You Can Save More Money

By refinancing to a lower interest rate, you can save more money in the long run.

For example, let’s say you currently have a student loan of $80,000 with an 8% interest rate and a 10-year repayment plan. You decide to refinance and qualify for a new loan of $80,000 with a 5% interest rate.

After refinancing, instead of paying $36,474.49 in interest with a 8% interest rate, you’d only need to pay $21,822.89, saving you roughly $15,000.

You Can Pay Off The Loan Quicker

Just like you can extend your repayment period through refinancing, you can shorten it if you want to pay off the loan quicker. This will mean that your monthly payments will be higher, but if your financial situation allows for this increase, it may be desirable for some borrowers.

You Don’t Qualify for Student Loan Forgiveness

Refinancing may be the way to go if:

You have private student loans, which do not qualify for loan forgiveness.

You do not have an income-driven repayment plan for your federal loans.

You do not work in a qualifying public service position for Public Service Loan Forgiveness.

Refinancing is done through private student loans. If you opt to refinance a federal student loan into a private student loan, you will lose the benefits that come with federal student loans. However, if you plan to refinance a private student loan, these benefits are not at risk.

Cons of Refinancing

You Can Lose Federal Borrower Protections

If you refinance your federal student loans, they will become private loans. This means that you’ll lose out on federal borrower protections, including the opportunity for loan forgiveness, more flexible repayment plans, and loan deferment and forbearance options.

You Can’t Get a Lower Interest Rate And/Or Monthly Payment

If you don’t have a high enough credit score or a cosigner with a strong credit history, you may not qualify for a lower interest rate and/or monthly payment. If this is the case, you shouldn’t refinance your student loans because you wouldn’t be gaining anything from doing so.

You’re Almost Done Paying Off Your Student Loans

If you only have a few more payments left on your student loans, it may be better to not refinance your loans. When you refinance your loans, you have to choose a new repayment plan that can extend the life of the loan, increasing the amount you have to pay.

Instead of refinancing, pay off your loan with your current plan.

Is Refinancing Student Loans Worth It? It Depends.

You should consider refinancing if:

You qualify for a lower interest rate or monthly payment.

You do not qualify for federal loan forgiveness.

It will save you money in the long run.

You should not consider refinancing if:

You are almost done with paying off your loans.

You do not qualify for more competitive terms than the ones you already have.

You are eligible for federal student loan forgiveness.

Closing Thoughts From the Nest

Consider the pros and cons of student loan refinancing to determine whether the decision is worth it for you in the long run.

If refinancing your student loans is beneficial to you, consider using Sparrow as a tool to see your loan refinancing options. You can compare personalized offers across 15+ different lenders, all for free.

Managing many student loan payments at once can be very difficult. That’s why student loan consolidation sounds so enticing. You can streamline your payments into one and make it easier on yourself. It sounds like the perfect solution. However, it’s essential to think about student loan consolidation pros and cons.

Before you start the application process, you should learn about the pros and cons of student loan consolidation so you can make the best decision possible. Lucky for you, this article is your guide to all things consolidation. Let’s get into it.

What is Student Loan Consolidation?

Student loan consolidation is the process of combining all your federal student loans into one. This is done through a Direct Consolidation Loan that you’ll apply for. A Direct Consolidation Loan is a form of Direct Loan offered by the government.

If you noticed that this sounds similar to student loan refinancing, you wouldn’t be the only one. Many people see consolidation and refinancing as the same thing. The reality, though, is that they’re pretty different. Here are a few differences.

You can only consolidate federal student loans. Meanwhile, you can refinance both federal and private student loans.

While an advantage of refinancing is the possibility of a lower interest rate, you probably won’t get that with consolidation. When you consolidate your loans, they will average all of your loan interest rates together and then round up to the nearest ⅛ percentage. This means it will most likely stay the same or go up.

When you consolidate, you’ll retain access to all of your federal benefits. Some loans, like the Federal Perkins Loans, need to be consolidated to access those benefits. Meanwhile, refinancing your federal loans would cause you to lose them.

Pros of Consolidating Student Loans

Simplifies Managing Your Debt

One advantage of student loan consolidation is it simplifies your debt payment. If you have multiple student loans, you understand how hard it can be to pay each one on time. By consolidating, you’ll only have one student loan instead of several. That way, you only worry about making a single payment per month.

Can Extend Your Repayment Term

When you consolidate, there is the possibility of getting an extended repayment plan. This extended plan can provide you the extra needed time to be able to pay off the loan. Plus, with an extended repayment, usually comes a lower monthly payment.

Can Lower Your Monthly Payment

As we mentioned, you might be able to lower your monthly payment when you consolidate. Typically, this will only happen if you get a longer loan term. This is because you’ll have more time to pay off the same amount of money, so you’ll pay less monthly.

For example, paying a $100 loan off in two months means making $50 monthly payments. If you extend the loan term to five months, then you’ll only pay $20 monthly. It’s the same concept with getting a longer loan term.

Cons of Consolidating Student Loans

You Could End Up Paying More

Unlike refinancing, you most likely won’t get an interest rate reduction through student loan consolidation. Your interest rate will either stay the same or go up. If you do get a higher interest rate, it would add to the overall cost of the loan and raise your monthly payments. So, you might have to pay more if you consolidate.

If You Consolidate Privately, You’ll Lose Federal Loan Benefits

When you consolidate privately, you will lose your federal benefits. This includes benefits like income-based repayment plans and loan forgiveness. So, you’ll want to think seriously about whether you’ll need these benefits or not. If you think you will, don’t consolidate privately.

You Could Pay More in Interest

As stated, when you consolidate, you could get a longer loan term. Although a longer term can be great, it does mean that you will pay more in the long run. Why? Because there will be more time for interest to build, and that interest will add to the overall cost.

For example, say you have a $30,000 loan with a 5% interest rate on a standard repayment plan of 10 years. Over those 10 years, you’ll pay an extra $8,184 in interest for a total of $38,184. If your loan term got extended to 20 years, then you’ll pay an extra $17,517 in interest for a total of $47,517.

FAQ About Consolidating Student Loans

Will consolidating my student loans hurt my credit?

No, Direct Consolidation Loans don’t have any kind of credit score requirement or even do a credit check. So, you don’t have to worry about anything popping up on your credit report. Your score will remain the same.

If you opt to refinance and consolidate privately, you will need to pass a credit check to qualify. This may temporarily hurt your credit score.

Does consolidating student loans lower your interest rate?

No, it does not. Your interest rate will most likely stay the same or go up. When determining your interest rate, the government takes the weighted average of all your loans’ interest rates and rounds it up.

Student loan consolidation and refinancing through a private lender, however, will likely get you a lower interest rate.

Is it better to consolidate or refinance student loans?

It depends on your situation since each has its pros and cons. Consolidating helps you better manage your debt, but you could end up spending more money. Refinancing can help you save a lot of money and manage your debt, but you would lose federal benefits. It’s really up to you and what your priorities are.

To help you make the decision, here’s a list of the top 4 refinance rates. Rather than searching for lenders one-by-one, we recommend starting the process with an automated student loan search tool. After you complete the free Sparrow application, we’ll show you the rates and terms you’d qualify for with 17+ premier lenders.

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

It’s a big decision to make, and student loan consolidation has its pros and cons. Be sure to take the time to think about it and figure out what’s best for you. That way, no matter what happens, at least you know you made the most well-informed decision.

If you choose to take a different route instead, like refinancing, use Sparrow to help you compare refinance rates across multiple lenders. The Sparrow application will match you with what you best qualify for from our partnering lenders. A lot of them offer great refinancing options. Plus, you’ll be able to refinance your federal and private loans together. To get started, fill out the Sparrow application.

If you’ve already refinanced your student debt once, you know just how much it can save you. For example, borrowers that use Sparrow to refinance save, on average, $17,000 over the life of their loan.

With that in mind, you may be curious if you can refinance more than once. And if so, how many times can you do it? Here’s what you need to know.

Can You Refinance Student Loans Twice?

You can refinance your student loan debt as many times as you’d like. While common to do it once, you may be able to save even more by refinancing again.

For example, let’s say you started with a $30,000 student loan balance at a 6.8% interest rate with a 10-year repayment term. You refinance when you’re fresh out of college to a loan with the same balance and repayment term, but a 4.25% interest rate instead. Your new loan will save you $38 per month, or around $4,551 over the life of the loan.

Now, let’s say you opted to refinance again one year into paying off that loan. Your balance is now $26,029.05, and there are 9 years left in your repayment term. You refinance to a new loan with a 3.5% interest rate and a 5-year repayment term. While your monthly payment would increase, you would save another $2,958 over the life of your loan.

Initial Loan

1st Refinance, immediately after college

2nd Refinance, 1 year after making payments on the first refinance loan

Starting Balance

$30,000

$30,000

$26,029.05

Interest Rate

6.8%

4.25%

3.5%

Repayment Term

10 years

10 years

5 years

Monthly Payment

$345

$307

$474

Total Paid Over the Life of the Loan

$41,429

$36,878

$28,411

By the time you refinance a second time, you will have already paid $3,684 toward your loan ($307 monthly payment x 12 months). However, including that amount, you will only pay $32,095 total after refinancing twice. Compared with your initial loan terms, you will save $9,334 over the life of the loan.

When to Consider Refinancing Multiple Times

While refinancing more than once can make for considerable savings, it’s important to consider a variety of factors before doing so. Here are a few instances in which it does make sense to refinance multiple times:

If the savings will be significant. Refinancing is intended to make repaying your debt more manageable or less expensive. If you can save a decent chunk of cash by refinancing again, it likely makes sense to do so. However, consider whether the savings is worth going through the refinancing process again.

If your credit score has increased. If your credit score has improved since the last time you refinanced, you will likely qualify for better terms or a more attractive interest rate. If it has not, however, it may be challenging to qualify for a better offer than what you currently have.

If the origination fees are either low or nonexistent. While the majority of student loan lenders don’t have origination fees, some do. If the origination fee is so high that it equals, or outweighs, what you will save by refinancing, it may not make sense to do so. However, if the origination fees are low, or if there is no origination fee at all, refinancing again will likely save you money.

If you want to release a cosigner. If your current loan has a cosigner, and does not allow for cosigner release, you may want to refinance again to release them from their cosigner obligations.

Is It a Bad Idea to Refinance Multiple Times?

Refinancing your student loans multiple times isn’t a bad idea if you are in fact receiving a better interest rate or terms.

Submitting a formal loan application will result in a hard credit check, however, which will temporarily hurt your credit score. If your credit score isn’t in a good place, refinancing again may not be in your best interest.

How Long Do You Have to Wait to Refinance Again?

Legally, there is no limit to the number of times you can refinance within a certain period of time. So, theoretically, you could refinance a million times if you wanted to.

However, most refinance lenders cap the number of times you can refinance with them. For example, some may limit you to one refinance per month or per quarter.

What to Consider Before Refinancing Your Student Loans

Before refinancing your student loans, consider the following:

The type of loan you have. If you have federal student loans, be sure to weigh the pros and cons of refinancing them prior to doing so. If you do, you will lose access to all federal loan benefits such as income-driven repayment plans and federal loan forgiveness.

Your interest rate. While you can score a lower interest rate by refinancing, you may have already hit the lowest possible rate you can get. To see if it’s even possible to qualify for a lower rate, complete the Sparrow application. This will allow you to compare prequalified rates side-by-side, giving you insight into what you may qualify for.

Think about your current financial situation. Refinancing to a shorter repayment term will likely cause your monthly payment to increase. Make sure you’re able to afford that payment prior to refinancing again.

The credit impact. Submitting a formal loan application will result in a hard credit inquiry, which will temporarily hurt your credit score. While your credit score will recover from the hit over time, it’s important to make sure refinancing makes sense before clicking “submit” on a formal loan application. Minimize the number of applications you submit, or do so within the recommended FICO and VantageScore timeframes so the inquiries are recognized as rate-shopping.