The average individual with a Masters in Social Work has around $68,000 to $76,000 in student loan debt. If you’re in the same boat, you’re not alone. To relieve the burden of student loan debt, consider pursuing loan forgiveness for social workers. Many federal forgiveness programs support individuals who work in public service, including social workers.

National Programs

The following loan forgiveness programs are for federal student loans only.

Public Service Loan Forgiveness

Public Service Loan Forgiveness (PSLF) is a loan forgiveness program for individuals who work in public service, including social workers, teachers, nurses, and more. If you have, or plan to have, more than 10 years of full-time employment in public service and have made 120 qualifying monthly payments to your federal student loans, you may be eligible for PSLF.

You must complete the PSLF application to qualify.

National Health Services Corp Loan Repayment Programs

If you are a licensed clinical social worker, you may qualify for one of the National Health Services Corp’s three loan repayment programs:

National Health Services Corp Loan Repayment Program: For licensed primary care clinicians who serve at least two years of service at an approved site in a Health Professional Shortage Area.

National Health Services Corp Substance Use Disorder Workforce Loan Repayment Program: For health professionals who serve in a Health Professional Shortage Area and improve access to Substance Use Disorder.

NHSC Rural Community Loan Repayment Program: For health providers who work against the opioid epidemic in an approved rural community.

Perkins Loan Cancellation

Public service workers who have taken out Perkins loans before 2017 might be eligible for Perkins Loan cancellation. To verify whether you are eligible, reach out to your school’s financial aid office for the next steps.

Income-Based Repayment Forgiveness

Beyond federal student loan forgiveness programs, social workers can also take advantage of income-based repayment forgiveness.

If you make 20-25 years’ worth of repayments on any of the aforementioned repayment plans, you may be eligible for the rest of your loan balance to be wiped out.

State-Based Programs

Each U.S. state offers at least one state-specific student loan forgiveness program, which social workers may be able to take advantage of.

For example, Kentucky has a 50/50 matching loan repayment program for healthcare providers who serve in underserved and rural areas. In New York, licensed social workers who work in critical human services areas can get up to $26,000 shaved off of their loans.

Other Ways to Find Relief

Beyond student loan forgiveness programs, you can find student loan relief through other means, such as student loan refinancing.

Student loan refinancing is the process of taking out a new loan, preferably with better terms, to replace your current loan. The new loan can have a lower interest rate or monthly payment to help make the loan more affordable. Here is a list of the top student loan refinance rates. In just three minutes, you can compare real and personalized student loan refinancing rates from 17+ lenders – for free – by using the Sparrow application.

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

For example, let’s say you have a student loan for $10,000 with a 10% interest rate and a repayment plan for 5 years. With your current plan, you pay $2,748.23 in interest. If you refinance your loan to have a 5% interest rate, you pay a total of $1,322.74 in interest, saving you around $1,400 in total.

To explore student loan refinancing offers, complete the free Sparrow application.

Being a military spouse requires a level of sacrifice some may never understand, and oftentimes placing your career on hold is one of them. While sometimes necessary to keep up with a life of frequent moves, it can create additional challenges when it comes to paying off student loans. That’s why it’s important to know your military spouse student loan forgiveness options.

Can Military Spouses Get Student Loans Forgiven?

Currently, there are no student loan forgiveness programs designed specifically for military spouses. However, military spouses can still receive loan forgiveness through conventional federal forgiveness programs.

For full-time teachers who have taught for 5 consecutive years at a low-income school or educational agency. If you taught secondary-level mathematics or science, or were a special education teacher, you can be eligible for up to $17,500 in loan forgiveness. All other subjects can receive up to $5,000 in loan forgiveness.

For registered nurses, nurse faculty, or advanced practice registered nurses who have attended a qualifying nursing school and work in a critical shortage facility or accredited nursing school. Recipients can receive up to 85% of their nursing loans forgiven.

For nurses who work in Medicare, Medicaid, or the State Children’s Health Insurance Program. Full-time nurses can receive up to $50,000 in loan forgiveness, while half-time nurses can receive up to $25,000.

Servicemembers Civil Relief Act

The Servicemembers’ Civil Relief Act allows military spouses to lower the interest rate on their loans to 6%, if the loan was borrowed before the service member entered active duty. While this program is not loan forgiveness, it can help lower your monthly payments. Qualifying service members include those in the Army, Navy, Air Force, Marine Corps, Coast Corps, reservists on active duty, and more.

Student Loan Refinancing

Student loan refinancing allows you to swap your current loan for one with a better interest rate or terms. In some cases, this can help lower your monthly payments, making keeping up with them a bit easier.

If you have federal loans that do not qualify for loan forgiveness, you can sometimes consolidate them to a qualifying loan type. For example, if you have Federal Family Education loans (FFEL), which do not qualify for federal loan forgiveness, you can consolidate them into a Direct loan.

Income-driven repayment is a federal loan repayment plan that bases your monthly payment based on your income. After making 20-25 years’ worth of qualifying payments, your remaining student loan balance can be forgiven

State-Sponsored Assistance Programs

Some states offer loan assistance programs for their residents. For example, Iowa offers the Teach Iowa Scholars program, which provides qualifying first-year Iowa teachers with $4,000 per year for teaching in designated shortage areas. New York offers qualifying social workers up to $26,000 in loan assistance through the NYS Licensed Social Worker Loan Forgiveness program.

Closing Thoughts From the Nest

As a military spouse looking for loan forgiveness options, be sure to exhaust all options available to you. While there are no specific loan forgiveness options for military spouses, there are plenty of programs you can still take advantage of.

If you owe more than 6-figures in student loans, you may feel overwhelmed by your debt. However, you’re not alone. In 2021, there were around 900,000 borrowers who owed $200,000 or more in student loans.

If you want to learn how to pay off $200k in student loans fast, you’re in the right place. Keep reading for the best strategies to wipe out your student loan debt balance.

Look for Student Loan Forgiveness Opportunities

Before finding ways you can pay off $200k in student loans using your hard-earned cash, you should always look for free money first. Exploring student loan forgiveness opportunities is key.

If you borrowed federal student loans, you may be eligible for student loan forgiveness. Here’s a few programs that you should explore:

Public Service Loan Forgiveness

The Public Service Loan Forgiveness program is for federal loan borrowers who work in the public sector. Whether you’re a volunteer, teacher, or nurse, you may be eligible for student loan forgiveness if you work for a qualifying U.S. federal, state, or local employer.

Here are some common professions that qualify for Public Service Loan Forgiveness:

Non-profit

Government

Lawyers

AmeriCorps

Peace Corps

Medical field

Loan Forgiveness Through Repayment Plans

Depending on your loan type, repayment plan, and the number of loan payments you’ve made, you may be able to have your student loans forgiven. If you have the Income-Based Repayment Plan, Pay As You Earn (PAYE) Plan, Income-Contingent Repayment Plan, or the Revised Pay As You Earn (REPAYE) Plan, you can qualify for loan forgiveness if you have made on-time and in-full payments for a specified amount of time.

Occupation-Based Loan Forgiveness

If you are in the Army National Guard, AmeriCorps VISTA, AmeriCorps State, or AmeriCorps NCCC, you may qualify for specialized loan forgiveness. Military service members can qualify for Public Service Loan Forgiveness, National Defense Student Loan Discharge, and more. Reach out to your military organization to see whatstudent loan forgiveness options you may have.

If you are a public school teacher who works for an eligible school, you may also be eligible for loan forgiveness. Generally, you need to have taught at a low-income school and made a minimum of 120 full and on-time payments. Some programs that you can look into are the Public Service Loan Forgiveness, Teacher Loan Forgiveness, and Perkins Loan Cancellation.

Borrower Defense

If you believe you were scammed or defrauded by your school and can prove it, you may be eligible to have your student loan balance wiped out entirely. You’ll need to file a claim with the Department of Education with evidence that you were deceived or misled by your school.

Refinance to a Lower Interest Rate

Before looking into student loan refinancing options, double-check that you do not have any opportunities for student loan forgiveness. If you refinance your student loans, you may lose eligibility for loan forgiveness in the future.

Loan refinancing is when you swap out your current loan with a new loan to pay off your debt. Generally, the new loan should have more favorable terms, such as a lower interest rate or monthly payment. This, in turn, can help you pay off your loans faster and save you money on interest.

Cut Back Expenses or Pick Up A Side Hustle

To pay off $200k in student loans, you can either increase how much you earn, reduce how much you spend, or do both. Generally, it is difficult for borrowers to cut back their expenses and pick up a side hustle, so don’t stress if that is you. Choose the strategy that works best for you.

If you’re hustling hard and looking for creative ideas to cut back on expenses or make more money, consider the following:

Do you have any paid subscriptions you forgot about? Try using a software like Rocket Money to catch any subscriptions you might be paying for without knowing it.

When was the last time you negotiated your bills? If it’s been more than a year, it’s time to call.

When was the last time you discussed your salary with your boss? While it might be an awkward conversation to have, it’s definitely in your right to talk about a pay raise.

Use Upside when purchasing gas. Not only will it tell you where the cheapest gas prices are, but it’ll give you cash back for purchasing gas (which is often a necessary expense for most individuals).

If you do not have any expenses to cut out, consider picking up a side hustle. Whether you decide to pick up a second job or explore freelance work, anything that brings an additional stream of income will help you.

Look at Your Company’s Benefits

Believe it or not, some employers will give you extra money to pay off your student loan debt. Reach out to your employer’s HR office and ask about any student loan payoff benefits they may offer. Or, if you’re applying for a new job, add in student loan repayment benefits when negotiating your salary and compensation package.

Use the Debt Avalanche Method

The debt avalanche is a popular method to tackle student loan debt. When using the debt avalanche method, you:

Pay the minimum payment for all of your outstanding debt, and;

Use your remaining money to pay off your debt with the highest interest rate.

The idea behind the debt avalanche method is to target your debt with the highest interest rate so you can spend less on interest in the long run.

For example, let’s say you are currently paying off three student loans: one of them has an interest rate of 10%, one has an interest rate of 7%, and the last one has an interest rate of 5%.

Using the debt avalanche method, you would pay off the minimum amounts for all of the loans, while directing any extra money to the loan with a 10% interest rate.

After the student loan with the 10% interest rate is entirely paid off, you would begin directing all of your money to the loan with the 7% interest rate, while making minimum payments on both the 5% and 7% loan.

How Long Will It Take to Pay Off?

To calculate how long it would take you to pay off $200k in student loans, you can use a student loan calculator. Student loan calculators allow you to adjust your monthly payment in different scenarios, allowing you to see how long different repayment plans would take.

Closing Thoughts From the Nest

While paying off $200k in student loans may seem like a daunting goal, it is definitely possible. By researching your options and being financially pragmatic, your student loan debt is something that you can overcome.

With President Biden’s student loan forgiveness program dominating news headlines as the federal courts debate the legality of his debt relief plan, you may be wondering, “What is student loan forgiveness?”

If that’s the case for you, you’re in the right place. Keep reading to learn about what student loan forgiveness is and what programs you might qualify for.

How Student Loan Forgiveness Works

Student loan forgiveness wipes out all or part of your remaining student loan balance for federal loans only. However, there are strict eligibility requirements to qualify for federal student loan forgiveness. In fact, most debt relief are only offered for public service occupations.

Student Loan Forgiveness Programs to Consider

Public Service Loan Forgiveness

Public Service Loan Forgiveness (PSLF) is a program that offers debt relief for qualifying individuals who work in public service, whether that be volunteer work, medical practice, or other public sector work.

To qualify for Public Service Loan Forgiveness, you must :

Have paid the minimum amount due on time for 120 payments (10 years total).

Have worked 10 years in a public sector role.

Have borrowed Direct Loans or consolidated their federal loans into Direct Loans.

Loan Forgiveness Through Repayment Plans

Certain federal repayment plans offer loan forgiveness if enough qualifying payments are made on the loan. While this may take substantially longer than federal loan forgiveness programs, borrowers will still be able to receive debt relief.

Income-Based Repayment

Income-based repayment (IBR) is a repayment plan where the maximum monthly payments are between 10% to 15% of your discretionary income.

You must have 20-25 years of qualifying payments under your belt to be eligible for loan forgiveness.

Income-Contingent Repayment

Income-contingent repayment (ICR) is a repayment plan that is (hence the name) contingent on your income. Your monthly payments are recalculated every year based on your family size, outstanding loan balance, and gross income. Generally, your monthly payments will be around 20% of your discretionary income.

You must have 25 years of qualifying payments to be eligible for loan forgiveness.

Pay As You Earn (PAYE)

Pay As You Earn (PAYE) is a repayment plan where your monthly payments are 10% of your discretionary income and capped at how much you would pay on a regular, 10-year repayment plan.

The main benefit of the PAYE repayment plan, however, is that the government will pay 100% of the unpaid interest on your subsidized loans for the first three years.

To qualify for PAYE, you must demonstrate financial hardship and have received a federal loan after October 1, 2007. You must then make 20 years of qualifying payments to be eligible for forgiveness.

Revised Pay As You Earn (REPAYE)

REPAYE is the revised version of PAYE that has slightly different terms. The monthly payments for the REPAYE plan are 10% of your discretionary income with no cap, meaning that you could be paying more than you would on a standard 10-year plan.

With this plan, the federal government will:

Pay 100% of the unpaid interest on your subsidized loans for the first three years; or

Pay 50% of the unpaid interest on your subsidized loans and unsubsidized loans after the first three years.

Anyone with federal loans can be eligible for the REPAYE plan. You must then make 20 years of qualifying payments to be eligible for debt relief for undergraduate loans, or 25 years of qualifying payments for graduate loans.

Specialized Loan Forgiveness

If you have a specialized career, you may be eligible for loan forgiveness programs, such as:

Army National Guard Student Loan Repayment Program: If you’re a member of the Army National Guard you may qualify to have $50,000 shaved off of your federal loans. You must have Direct, Perkins, or Stafford loans.

Teacher Loan Forgiveness Program: If you are a full-time teacher who works in a low-income school or other eligible educational agency, you may be eligible for $5,000 to $17,500 in loan forgiveness. You must have worked full-time for a qualifying position for five consecutive years, and have Direct or Stafford loans.

Segal AmeriCorps Education Award: If you were a part of the AmeriCorps VISTA, AmeriCorps State, or AmeriCorps NCCC, you may be eligible to receive up to the maximum Pell Grant award to pay off your federal student loans.

Borrower Defense

If your school significantly deceived, defrauded, or scammed you, you may be eligible for borrower defense to loan payment forgiveness.

If you qualify for borrower defense, you will receive loan discharge. Loan discharge, unlike loan forgiveness, immediately stops your loan payments and may even allow you to receive a refund on your repayments.

To have your student loans discharged through borrower defense, you need to file a claim to the Department of Education with evidence that you were deceived or misled by your school.

Who Qualifies for Student Loan Forgiveness?

Eligibility for student loan forgiveness depends on the program being offered.

If you work in the public sector and have made enough qualifying payments, you may be eligible for the Public Service Loan Forgiveness program. On the other hand, if you are a teacher who’s worked for five consecutive years at a low-income school, you may be eligible for the Teacher Loan Forgiveness program.

If you feel that your career may qualify for loan forgiveness, be sure to check your eligibility with the Federal Student Aid office.

Closing Thoughts From the Nest

While the future of the Biden administration’s student loan relief program is still uncertain, you can subscribe to the Department of Education’s email updates to stay up-to-date with the latest information. Beyond Biden’s comprehensive loan forgiveness plan, remember there are still opportunities for you to have your federal student loans forgiven with existing programs.

While there are both drawbacks and benefits of paying off student loans early, the decision ultimately depends on your financial priorities and standing.

Should I Pay Off Student Loans Early?

Ask yourself the following questions:

#1: Do you have at least 3-6 months’ worth of emergency funds?

Having a rainy-day fund that can last you roughly 3-6 months is crucial in being prepared for unexpected circumstances. Before directing your extra money to pay off your student loans, make sure you are financially prepared for any emergencies.

#2: Are you saving for retirement?

While retirement may seem far away, investing in your retirement while young is crucial to having long-term financial security. If your retirement fund is lacking, consider prioritizing it first.

Once you’re in the position to pay off your student loans while still adding to your retirement fund, then you may want to start directing some extra money to your student loan payments.

#3: Have you paid off all high-interest debt?

High-interest debt is extremely volatile, as the initial amount of money you borrowed can quickly grow larger. Any high-interest debt you have should be a priority to pay off so that the consequences of compound interest do not work against you.

#4: Do you have a “sufficient” income?

If you are able to comfortably make larger student loan payments, you’re in a good spot to pay off your loans early. However, if doing so will place some strain on your financial situation, it might not be the best idea. You’ll want to be able to meet your basic expenses like your bills, rent, and car payments first.

Benefits and Downsides of Paying Off Student Loans Early

Before making your final decision, carefully weigh the pros and cons.

Benefits of Paying Off Student Loans Early

Save Money on Interest

Student loans collect interest over time. If you pay off your student loans early, you’ll pay less in interest, saving more money overall.

For example, let’s say you have a loan of $10,000 with a 5% interest rate and a 10-year repayment plan. If you opted to pay off the loan early by adding an extra $200 to your monthly payment, you’d pay off the loan in 3 years and pay a total of $10,850, saving you $1,878 and 7 years of your time.

Lower Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is used to compare how much you earn (your gross income) against how much you owe (your total debt). [DTI = Monthly Debt ÷ Gross Monthly Income]

For example, let’s say your total debt payment per month is $3,500, including expenses like your mortgage, student loan payments, and credit card bills. Your gross monthly income, or how much you earn every month before any deductions, is $6,000.

Using the formula above, we would calculate $3,500/6,000, which is roughly 58%.

A “healthy” DTI is 36% or less. Having a DTI over 50% indicates that you owe more than half of what you make, which is a very poor ratio that lenders do not look kindly upon.

If you pay your student loans off early, you can lower your DTI quickly. Having a lower DTI will help you secure lines of credit more easily, such as a mortgage, a new credit card, and more.

You Can Focus on Other Financial Goals

If you knock out your student loans early, you can focus on other financial goals like buying a house or saving for retirement.

Downsides of Paying off Student Loans Early

Monthly Payment Will Be Higher

To pay off your student loans early, your monthly payment must be higher. For example, let’s say that you are paying $250 per month to pay off your student loan in two years. If you want to pay your loans off in just one year, your monthly payment must double to $500 because your repayment plan is halving.

If affording a higher monthly payment would be nearly impossible, or put you in a risky financial situation, it may be best to hold off.

You Won’t Be Eligible for Student Loan Forgiveness

The federal government offers several student loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or the Income-Driven Repayment Forgiveness (IDRF).

If you are eligible for a federal student loan forgiveness program that requires you to make payments for a certain amount of time, you should not pay off your student loans early. Doing so could make you ineligible for forgiveness.

If you are not eligible for student loan forgiveness, paying your balance off early would be wise.

This only applies to borrowers with federal student loans, as private student loan borrowers do not have the option for loan forgiveness.

You May Not Be Able to Focus on Other Financial Goals for the Time Being

By directing more money towards paying off your student loans, you may not have enough money to focus on any other financial goals, like saving for a down payment on a home or contributing to a Roth IRA. So, consider your financial priorities before directing all extra funds toward student loan payoff.

Is It Worth It To Pay Off Student Loans Early?

Yes, it is worth it to pay off your student loans early if you are financially stable enough to do so. If you can afford to put more money onto your loan, it will save you both time and money in the long run.

However, there are instances when it is not worth it to pay your loans off early. For instance, if you qualify for federal student loan forgiveness, have debt with a higher interest rate, or do not have an emergency fund, it might be more advantageous to prioritize other aspects of your finances.

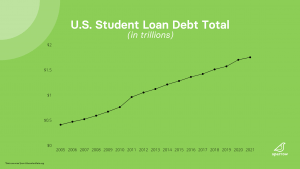

The total student loan debt, between both federal and private loans, is $1.75 trillion. If your debt is contributing to this total, it’s time to pay it off.

Whether you borrowed private loans, federal loans, or a mix of both, deciding which student loans to pay off first can be difficult. However, it’s important to keep in mind that there is no single one-size-fits-all solution.

Instead, let’s explore a few tactics that can help you save money. This will help you determine which student loans to pay off first, based on your unique financial circumstances

Option #1: Pay Off Private Student Loans First

Private student loans are offered by commercial lenders like banks and credit unions. These organizations are autonomous, meaning they have the discretion to set interest rates, repayment plans, and borrower protections for loans.

Generally, in comparison to federal loans, private loans have less advantageous terms, with no option for loan forgiveness, higher interest rates, and fewer repayment plans.

If the lack of flexibility or the higher interest rates for your private loans is a cause of concern, pay those loans off first. By doing so, you are essentially targeting the “weightier” portion of your debt.

Additionally, consider refinancing your private student loans if it’s an option. Refinancing is the process of borrowing a new loan to pay off your current debt with better terms. This can lower your interest rate and monthly payments, which will be beneficial in the long-run. Keep in mind that you will need a relatively strong credit score to qualify for loan refinancing.

Option #2: Pay Off High-Interest Student Loans First

When Einstein said, “He who understands [compound interest], earns it. He who doesn’t, pays it,” he wasn’t kidding. The debt avalanche method is most effective for minimizing the costs of compound interest, which will save you the most money in comparison to other debt payoff benefits.

With this method, you’ll make minimum monthly payments on all loans while making surplus payments on the loan with the highest interest rate. Then, once you’ve paid off the highest interest rate loan, you’ll carry that payment amount to the next highest interest rate loan.

For example, let’s say you have two student loans:

Loan A: $10,000 balance, 5% interest rate, 10-year repayment term

Loan B: $5,000 balance, 3% interest rate, 2-year repayment term

In this scenario, you would make surplus payments on Loan A while still making minimum payments on Loan B. Doing so would minimize the interest costs for Loan, given that it will accrue a greater amount in interest than Loan B.

Option #3: Get Rid of Small Loans First

Targeting smaller loans is another debt payoff strategy known as the snowball method. The logic behind this method is to get rid of the loan with the lowest balance first.

The snowball method is relatively simple. First, organize your loans based on the total amount, without regard to the interest rate. Then, make paying off the smallest loan your priority. After the smallest loan is paid off, target the next loan in line.

For example, let’s say that your debt consists of the following:

Loan A: $5,000 balance, 3% interest rate

Loan B: $2,500 balance, 6% interest rate

Loan C: $3,500 balance, 8% interest rate

In this scenario, you would pay off Loan B first, given that it has the smallest balance.

While the snowball method isn’t the best repayment option in terms of saving the most money possible, you’ll be able to knock out individual loans quicker and have more upfront victories. For some, these upfront victories are what motivates them to stay consistent with their debt payoff journey.

Which Debt Payoff Strategy Will Save You the Most Money?

The debt avalanche method, where you target your high-interest loans first, will save you the most money. This is because you’re targeting debt with the highest interest rate, which will grow the fastest.

However, even if the debt avalanche method will save you the most money, it may not be the most optimal way to repay your debt. According to a study done by Northwestern’s Kellogg School of Management, borrowers who use the snowball method are more likely to pay off all of their debt than borrowers who use other methods.

Closing Thoughts From the Nest

As you consider debt payoff strategies, remember that there is no “right” answer. Instead, think about what best fits your financial situation.

If it’s less financially straining to pay off smaller loans first, use the snowball method. If you want the most bang for your buck and are confident you will be able to stick to a plan, use the avalanche method. In the end, everything depends on what you feel is best for you.

According to the Education Data Initiative, around 15% of student loans are in default at any given time.

If you are in student loan default, it’s understandable to feel overwhelmed and discouraged. However, don’t lose hope. There are many ways to financially recover from it.

A student loan default happens when you fail to repay a loan according to the terms outlined in your loan contract (also known as a promissory note).

What Happens Before Default?

Before a federal student loan default, your loan enters into a stage called delinquency. You enter into loan delinquency when you miss one federal student loan payment.

While your federal student loan is delinquent, you still have the opportunity to:

Switch repayment plans to receive a lower monthly payment

Contact your loan servicer to discuss your next steps as soon as you enter federal loan delinquency. It is crucial to take advantage of the federal borrower protections you have while you are delinquent so you will not default on your loan.

On the other hand, private student loans do not enter delinquency after a missed payment. They simply default after you miss the number of payments outlined in your promissory note. Contact your loan servicer to discuss what options you have after missing a payment. Depending on your loan, you may have to enter loan deferment/forbearance, or lower your monthly payment temporarily.

When Does a Student Loan Enter Default?

Federal and private student loans enter default at different points.

Federal student loans enter default if payment has not been made for 270 days, or around around nine months of missed payments. Defaulting on a federal student loan makes you ineligible for forbearance and deferment, repayment plans, and applying for any other federal student loans.

Private student loans usually enter default after you miss three monthly payments, or if payment has not been made for 90 days. They can also enter default if you declare bankruptcy, default on another loan, or pass away. However, not all loans default after three missed payments.

Always read the fine print on your promissory note to be aware of the specific default timeline for your loan.

How to Know if Your Student Loans are in Default

To verify whether your student loans are in default or not, you have the following options:

Contact your loan servicer. This is the best way to determine whether your loans are in default, as your servicer will be able to provide you with up-to-date information.

For federal student loans: Log into your Federal Student Aid account and check whether or not your loans have entered into default. You may be able to find similar information by logging into your private student loan account as well.

Check your credit report. Your credit report will list all federal and private student loan defaults. However, this may not be the most accurate way to check because credit reports are not constantly being updated.

What Happens if You Default on a Student Loan?

Student loan default can impact you in the following ways:

Your credit score is damaged.

Entering student loan default and missing loan payments will be reflected on your credit history for the next seven years. Because your credit score will be significantly impacted, your chances of qualifying for new lines of credit may be extremely difficult (and in worst cases, impossible).

You’ll owe more money.

Despite being in loan default, late fees and interest will continue to be applied to your debt. Debt collection agencies may also charge collection fees, adding to the amount of money you owe. Try to get your loan out of default as quickly as possible to avoid incurring additional costs.

You may be contacted by debt collectors.

A collection agency is a company that loan servicers use to recover loans in default.

If you default on a federal loan and make no actions for payment arrangements, loan servicers can place your loan with a collection agency. Defaulted private loans are considered “uncollectible,” or “charged-off,” and can be sold to a collection agency.

Once your defaulted loan is in the hands of a collection agency, debt collectors can contact you to recover your delinquent funds. Oftentimes, debt collectors will use aggression or scare tactics to coerce you into paying off your debt.

That said, debt collectors are legally obligated to follow the Fair Debt Collection Practices Act, which provides borrowers certain rights. If any of your rights are violated, submit a complaint to the Consumer Finance Protection Bureau.

The federal government may withhold your wages, tax refunds, and/or federal benefits.

To collect on federal student loans, your loan servicer has the legal discretion to withhold your wages, tax refunds, and government payments. In addition to garnishment, you will not be eligible for any federal financial aid or federal borrower benefits.

Your loan servicer may sue you.

Unlike federal student loans, private student loan servicers cannot garnish your wages or tax refunds. Instead, however, they have the legal discretion to take you to court. If you are sued by your loan servicer, the court can rule in their favor and require you to give up your bank accounts, paychecks, or any capital to pay off your debts.

Your professional license can be suspended.

License suspension laws vary from state to state, but bear in mind that any licenses you have (ex. professional license, driver’s license, etc.) can be suspended if you default on your student loans. While this may be an extreme case, it is still possible.

How to Recover from a Student Loan Default

If you have defaulted on a student loan, do not feel discouraged. You still have many opportunities to recover from a student loan default.

How to Recover from Federal Student LoanDefault

If you want to recover from a federal student loan default, consider the following options.

Rehabilitation

Usually, student loan rehabilitation is the best way to recover from federal student loan default because it removes the default from your credit report (though late repayments will remain).

Contact your loan servicer to inquire about loan rehabilitation.

Make nine consecutive monthly payments that are 15% of your discretionary income. You may request a lower amount if need be.

Note, however, that loan rehabilitation is a one-time opportunity.

Consolidation

Student loan consolidation is when you merge your defaulted loan(s) and current loan(s) into oneDirect Consolidation Loan.

To consolidate your defaulted federal loans, you need to:

Agree to repay the new Direct Consolidation Loan under an income-driven repayment plan.

Make three consecutive, on-time, full monthly payments on the defaulted loan.

Enroll in Fresh Start.

What is Fresh Start?

Fresh Start is a new federal program that aims to help defaulted borrowers. The program will begin in December 2023, a year after the COVID-19 payment pause ends.

Through Fresh Start, borrowers will temporarily recover student aid benefits and have the opportunity to get out of loan default.

Federal Student Aid (FSA) will reach out to you in the coming months if you are eligible to participate in Fresh Start. Therefore, you’ll want to make sure your contact information is up-to-date with your loan servicer.

Which Is Better for a Federal Student Loan Default: Loan Rehabilitation or Loan Consolidation?

Between federal loan rehabilitation and loan consolidation, there is no “right” answer. Instead, you should examine which option best meets your financial needs.

That said, there are a few things you should consider as you make your decision:

Loan rehabilitation is a one-time opportunity. If you fail to rehabilitate your loan(s) the first time around, you will not be able to do it again.

Loan rehabilitation requires nine monthly payments, while loan consolidation only requires three monthly payments to qualify.

Loan rehabilitation removes the loan default from your credit history, though any reported missed payments will remain. Loan consolidation does not remove your default.

The following chart details the benefits you gain from loan rehabilitation and loan consolidation.

Benefits

Loan Rehabilitation

Loan Consolidation

Loan Deferment

Yes

Yes

Loan Forbearance

Yes

Yes

Eligibility for Federal Financial Aid

Yes

Yes

Repayment Plans

Yes

Yes

Loan Forgiveness

Yes

Yes

Removal of Default from Credit History

Yes

No

How to Recover From Private Student LoanDefault

Unfortunately, private student loans don’t offer the same recovery options as federal student loans. You will need to contact your lender to discuss options for getting out of loan default. You may be able to negotiate a resolution or work out a payment plan that works for your financial needs.

If you need additional assistance, consider contacting a student loan lawyer.

How to Fix Your Credit After Defaulting

Take the following steps to fix your credit after defaulting on student loans:

Get out of default.

The first thing you should do to repair your credit after a default is ensure that you are completely out of default. While getting out of default won’t instantly fix your credit score, it’s the first step in getting it back up.

Pay off your debts.

In addition to paying off your defaulted loan, you will want to stay on top of paying off any other debts you may have (credit card debt, home mortgage, etc.) Having less debt will lower your debt-to-income ratio, which in turn will help raise your credit score.

Do not open new lines of credit.

While you might consider borrowing a personal loan to pay off your student loans, experts advise against this. Borrowing more money will only put you in further debt. Instead, use your current resources to manage your debt balances.

Closing Thoughts From the Nest

While defaulting on a student loan may feel like the end of the world, you can still recover from it. The best thing to do is to attempt to get out of it. Contact your lender or loan servicer as soon as possible to set up payment arrangements that work for you. In addition to that, remember your borrower rights if you are contacted by debt collectors.

If you’re studying in California, where 20% of discharge applications come from, student loan discharge programs may be familiar to you. However, the majority of borrowers haven’t heard of them.

While student loan forgiveness programs are more well-known, student loan discharge programs are another great way to have your student debt wiped from existence.

So, while student loan discharge programs are fairly unknown, shining a light on them is important as they could save you thousands of dollars. Let’s take a look at what student loan discharge programs are and the top programs you may qualify for.

What is Student Loan Discharge?

Student loan discharge programs remove your obligation to repay your debt. While similar to student loan forgiveness programs, discharge is typically only granted under extenuating circumstances. Forgiveness programs, on the other hand, are often granted based on your career or service to a particular industry.

For example, you may have your student loan debt forgiven after working in public service for a certain number of years, while your debt would be discharged for something like death or a disability.

Additionally, forgiveness programs are for federal student loans only, while both federal and private student loans are eligible for discharge (pending that you meet the eligibility criteria).

Top Student Loan Discharge Programs You May Qualify For

Closed School Discharge

As the name suggests, closed school discharge is aimed to remove the obligation for students whose school closed while they were still enrolled. To be eligible for a 100 percent discharge, you must meet the following criteria:

You must have been enrolled in the school when it closed, or you were approved for a leave of absence when your school closed;

If your loans were disbursed before July 1, 2020, then your school must have closed within 120 days after you withdrew; or

If your loans were disbursed on or after July 1, 2020, then your school must have closed within 180 days after you withdrew.

If you find yourself in similar circumstances to these criteria, you could be eligible for the Closed School Discharge. In the case that you are eligible, the Secretary will automatically send you an application you can submit to your loan servicer. Or, you can contact your loan servicer directly about the application process.

Borrower Defense to Repayment Discharge

This program is provided to students who have attended schools that have either misled them, or participated in activities that violated certain state laws. For an application to be accepted, you must be able to demonstrate that the school violated state law related to your loan or to the educational services provided. If you believe this criteria meets your situation, you can fill out an application here.

Total and Permanent Disability Discharge

The Total and Permanent Disability Discharge program (TPD) is for anyone who has become totally and permanently disabled. It relieves you from having to repay any federal loans. In order to qualify, you must provide documentation from one of the following sources:

The U.S. Department of Veterans Affairs;

The Social Security Administration; or

A Physician

Many private lenders also offer this discharge, but make sure to contact your lender directly to verify. If you are unable to complete the application on your own, you are able to have a representative apply on your behalf and help throughout the TPD discharge process.

Discharge Due to Death

If a student loan borrower dies during the duration of their student loans, it will be discharged. Likewise, a parent’s PLUS loan will be discharged if your parent dies.

FAQ About Student Loan Discharge

What happens if your student loans are discharged?

According to the Department of Education, a discharge of federal student loans implies that:

You will no longer be obligated to repay the loan,

You will receive a reimbursement for any payments made either voluntarily or through forced collection, and

The discharge will be reported to credit bureaus to delete any adverse credit history associated with the loan.

Essentially, your existing student loan gets deleted from your student loan account.

What is the difference between student loan forgiveness and discharge?

Both student loan forgiveness and discharge programs have similar end results, however they are quite different in the technicalities. Loan discharge programs immediately stop the borrower from having to repay the student loans, whereas a student loan forgiveness program implies that the borrower must repay the debt until their application is approved or until the borrower meets the necessary criteria. Additionally, certain discharges entitle borrowers to receive a refund of previously made payments on the loan.

Are discharged loans removed from your credit report?

Yes. When your loans are successfully discharged, it will be reported to the appropriate credit bureaus to delete any student loan related credit history.

Final Thoughts from the Nest

Now, with this knowledge of discharge programs, you can be confident that you know the general landscape for any relief programs. If you do not qualify for any discharge programs, check your eligibility for student loan forgiveness programs.

It’s the talk of the nation. The Biden Administration announced that it will be forgiving billions of dollars in student loan debt.

While this news is exciting, it’s a little nerve-wracking at the same time. You might wonder if you even qualify for student loan relief based on the requirements. What even are the requirements for this?

So, we’ve gathered everything we know and everything you need to know about Biden’s student loan forgiveness actions. Let’s get into it.

Who Qualifies for Biden’s Student Loan Forgiveness?

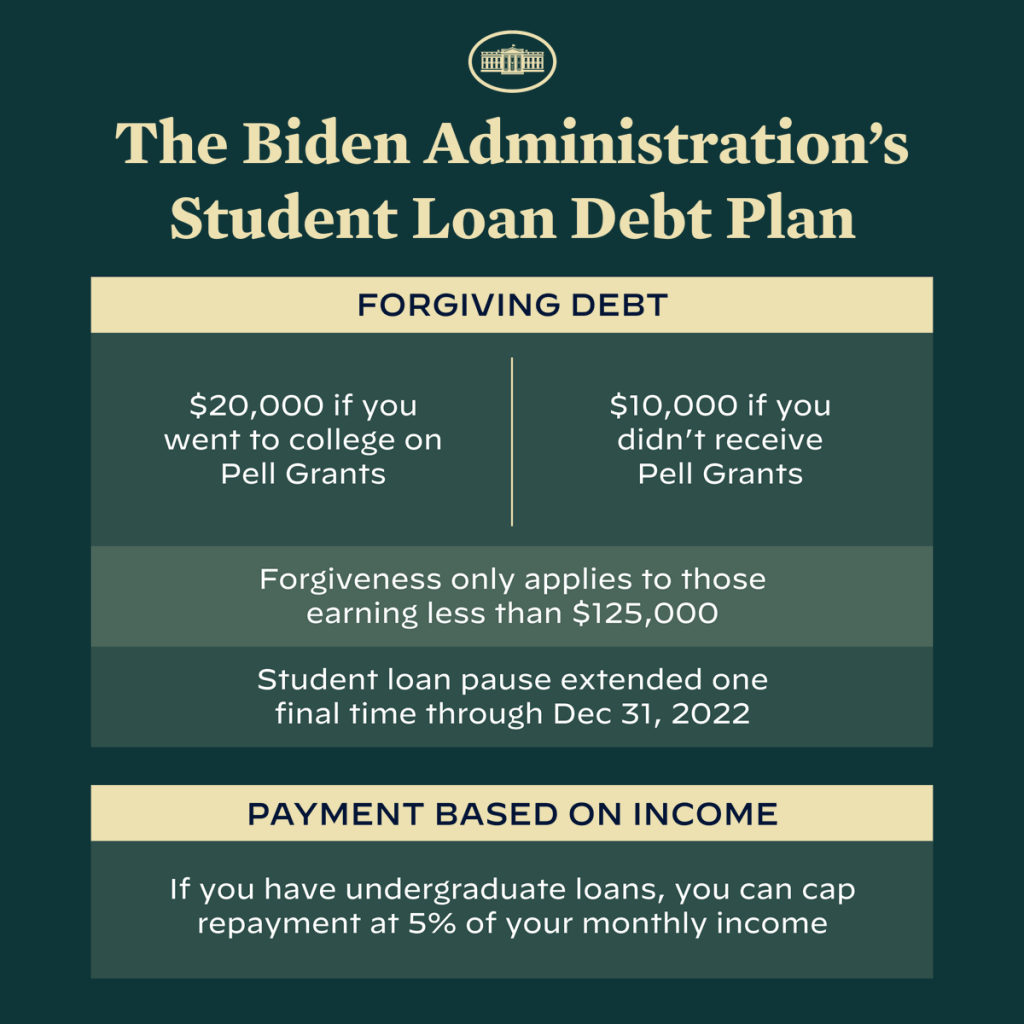

To qualify, you must have federal student loans that were disbursed no later than June 30, 2022. Qualifying loans include most federal loans like Direct Loans and Parent PLUS Loans. It’s unknown whether Federal Family Education Loans will also qualify for loan cancellation right now, but they might be able to later on. On the other hand, since this is a federal program, private loans are not eligible.

Additionally, you have to meet the income requirements the government has set forth to be eligible. Single individuals who earn under $125,000 per year are eligible. Couples who file taxes jointly and earn less than $250,000 per year are, too. Finally, heads of households who earn less than $250,000 per year are also eligible. From what we know, the information about your income will not come from the year 2022. The government will look at your income from the years 2020-2021.

Another thing you’ll want to look into is if you’ve ever received a Pell Grant. If you have, then you could get an extra $10,000 forgiven from your loans.

As you can tell from the information above, your eligibility is largely based on your income. Because of that, you’ll want to check your 2020 and 2021 tax returns to see if you meet the income requirement. The government may look at either or both tax returns to determine if you qualify. Make sure to save copies of your tax returns in case you need proof of income for the application.

To apply, you’ll need to do so online. Currently, the application is not available, but it will be by early October. The federal government advises borrowers to apply by November 15 to receive relief before the forbearance period ends on December 31.

Remember that the President extended the pause on loan payments for the final time. Borrowers will be expected to start making payments again on January 1, 2023.

How Will I Know if I Had a Pell Grant?

You may wonder if you’re eligible for the additional forgiveness if you previously received a Pell Grant. The good news here is as long as you received one at some point, you could have extra money forgiven. It won’t matter if you only had the grant for one year, got only a partial grant, or when in your college career you received it. As long as you have been or are a recipient, you should be good.

Don’t worry, if you forgot whether you received a Pell Grant in the past, you aren’t alone. If you’ve had or have a Pell Grant, it will already be on file and come up in your FAFSA account. Once you log onto your FAFSA account, it should show up on your dashboard under “My Aid”.

The section “My Aid” breaks down all the aid you’ve gotten for school. If you click on more details, you’ll get a more detailed breakdown of the loans and grants you’ve received. Your Pell Grant should show up there.

You’ll also want to save any documentation related to your Pell Grant like your financial aid award letters. That way, if you need it in the application process, you’ll already have it on hand.

Get Notified About Student Debt Relief Updates

As this was recently announced, there are still more details that are yet to come. To stay on top of student debt relief updates, sign up for email updates from the Department of Education. You can also check back on the FAFSA website for more information as it’s released.

Final Thoughts from the Nest

There is still a lot to learn about the program. But, from what we do know, this can help you find relief from your student loan debt. Be sure to sign up for the updates to stay on top of everything and be notified when the application goes live. In the meantime, gather all the documents that you need so you’re prepared for the application.

If you have private student loans, you may be bummed because you aren’t eligible for this. While those loans may not be eligible for this program, you can still save money on them by refinancing. By completing the Sparrow application, we’ll match you to the refinance loan options you best qualify for from our 15+ partnering lenders.

Making that last debt payment can feel liberating. The balance finally hits zero, and a weight is lifted off your shoulders. While an incredible accomplishment, you may notice a drop in your credit score, leaving you to feel quite defeated. It’s normal to wonder, “Why has my credit score dropped after paying my student loan? Isn’t that a responsible thing to do?” It does sound a bit backwards, huh?

However, it makes more sense when you understand how your credit score is calculated. Here’s why your credit score might drop after paying off debt.

How Your Credit Score is Determined

Your FICO credit score is calculated using five different factors: payment history, amounts owed, length of credit history, credit mix, and new credit. Each factor is weighed differently when calculating your score.

Payment History (35%)

To evaluate how risky lending to you might be, lenders will look at how you’ve handled credit in the past. If you have a spotless record, you’ll likely do well in this category. If your credit history is checkered with late or missed payments, however, you may lose some points here.

Amounts Owed (30%)

Having outstanding balances doesn’t necessarily make you a risky borrower to lend to. However, using a high percentage of your total credit limit is an indicator that you may be overextending yourself financially.

For example, if you have a total of $20,000 of available credit, and you’re using $19,000 of that, you may appear to be struggling financially. On the other hand, if your total available credit was $50,000, owing $19,000 wouldn’t be so bad.

In a lender’s eyes, having a high outstanding balance in comparison to your total credit limit puts you at a higher risk of defaulting on any one of your loans. Thus, a high credit utilization ratio will impact your credit score.

(Note: “Amounts Owed” is often referred to as credit utilization.)

Length of Credit History (15%)

Generally speaking, the longer your credit accounts have been open, the better your score may look in this category. Simply put, a long history of effectively managing your credit shows lenders you’re capable of handling credit responsibly.

Credit Mix (10%)

FICO scores also take into account your credit mix, or the variety of credit accounts you have (ie. credit cards, student loans, mortgage loans, retail accounts, etc.). While you don’t need to have an account open in each category, having a mix of credit accounts shows lenders you’re able to manage multiple lines of credit responsibly.

If you do have a mix of credit accounts and manage them effectively, it can give your score a boost.

New Credit (10%)

Opening several new lines of credit in a short period of time can be an indicator that you’re struggling financially. Thus, opening too many new lines of credit can hurt your score.

Why Your Score Drops After Paying Off Debt

While paying off debt is certainly something to be proud of, it may not reflect positively when it comes to your credit score. Here’s why:

It Can Change Your Credit Utilization Ratio

Let’s say you have three credit cards, each with a $10,000 limit. They’re set up as follows:

As a result, you’d have a credit utilization ratio of 40% (12,000 total outstanding balance / 30,000 total credit limit).

Now, let’s say you decide to pay off and close Card C. Your new credit utilization ratio would be 55% (11,000 total outstanding balance / 20,000 total credit limit).

By closing Card C, the credit limit associated with it is no longer factored into your credit utilization ratio. Thus, the new ratio of your outstanding balance to your total credit limit actually ends up being higher than it was before.

In some cases, closing an account can lead to a higher credit utilization ratio, as it changes the amounts owed in comparison to the total credit limit. This, in turn, will negatively impact your score.

It Shortens the Length of Credit History

When you close a line of credit, the credit history associated with it goes out the window. In the case of revolving credit, such as a credit card, this happens when you close a card. With student loans, this happens when you pay off the balance.

A few months after you make that final payment on your student loans, it will no longer be an active line of credit. The credit history associated with it, whether positive or negative, will be removed. Depending on how long you’ve had the account open in comparison to your other lines of credit, it could shorten your credit history.

For example, let’s say these are the three lines of credit you currently have:

Student Loan A: Borrowed 15 years ago Student Loan B: Borrowed 11 years ago Credit Card: Opened 10 years ago

In this scenario, the average age of your accounts is 12 years (15 + 11 + 10 / 3). If you paid off Student Loan A, the average age of your accounts would decrease to 10.5 years (11 + 10 / 2).

The credit history you had from Student Loan A gets wiped from your record, and your credit history is calculated based on the other lines of credit you have active.

It Could Change Your Credit Mix

If you have both revolving credit (like credit cards) and an installment loan (like a student loan), paying off your student loans will shift your credit mix. This could negatively impact your FICO score.

Will Biden’s Student Loan Forgiveness Impact Your Credit Score?

While President Biden’s student debt forgiveness will provide relief to millions of borrowers, it may wind up hurting your credit score temporarily for the reasons discussed above. And while the impact to your score pales in comparison to the relief provided, it’s important to understand why and how your score may drop so you know what to expect.

How Long It’ll Take for Your Score to Recover

If your credit score drops after paying off debt, don’t fret. While quite the bummer, it typically takes around 1-2 months for your score to bounce back (if everything else remains the same).

In the meantime, consider other ways to increase your credit score. Continue to use other lines of credit responsibly, and check on your score periodically to see if it increases as expected.

Final Thoughts from the Nest

While frustrating to see your credit score drop after paying off your student loans, it’s normal. Continue to practice healthy financial habits, and your score should bounce back in no time.

If, after a few months, your score is still the same, consider examining your full credit report to check for errors that may be preventing your score from recovering.

Since 1980, the cost of a college education has nearly tripled, even after adjusting for inflation. Yet, federal aid hasn’t kept up.

So, during his presidential campaign, Joe Biden promised to cancel $10,000 of federal student loan debt per borrower.

In August, he followed through with his promise, announcing up to $20,000 in forgiveness for eligible borrowers. While his plan will provide relief to millions, there are some borrowers that do not qualify.

Whether you don’t qualify due to your income or the type of loans you have, there are other student loan forgiveness programs available that you should consider.

Who Qualifies for Biden’s Student Loan Forgiveness?

Before completely writing off your eligibility, let’s review who qualifies for President Biden’s student loan forgiveness. To qualify, you must:

Have federal student loans

Make less than $125,000 per year, or less than $250,000 per year if married

If you received Pell Grants while in college, and meet the above criteria, you will receive $20,000 in student debt forgiveness. If you did not receive Pell Grants while in college, but meet the above criteria, you will receive $10,000 in student debt forgiveness.

Private student loans are not eligible for student loan forgiveness.

What to Do if You Don’t Qualify for Student Loan Forgiveness

If you don’t qualify for President Biden’s student loan forgiveness, there are other options you should consider.

Other Student Loan Forgiveness Programs

If you’re still itching for your student debt to be wiped out, or at least a portion of it, we don’t blame you. Consider other student loan forgiveness programs, such as the following:

Public Service Loan Forgiveness

Public Service Loan Forgiveness, or PSLF, is a government program intended to ease the burden of student loan debt for eligible public service workers. To qualify, you’ll need to have made 120 on-time, qualifying monthly payments on a Direct loan, on a qualifying repayment plan, while working for a qualifying employer.

Qualifying roles include, but are not limited to:

Teachers, staff members, and administrators at public schools

Law enforcement officers at the federal, state, or local level

Social workers at public service agencies

General employees at federal, state, or local agencies

Military servicemen

Public health professionals such as nurses, doctors, or administrators

Employees at 501(c)(3) organizations

Full-time volunteers at AmeriCorps or PeaceCorps organizations

If you do qualify, your remaining loan balance will be forgiven.

Teacher Loan Forgiveness

Teacher Loan Forgiveness is a federal program providing teachers with debt relief. To qualify, you must be a highly-qualified teacher that taught at a low-income school or educational service agency for at least five consecutive school years.

The amount forgiven depends on the subject you teach:

Full-time, secondary-level science or math teachers: Up to $17,500

Special education teachers: Up to $17,500

Other subjects: Up to $5,000

Nurse Corps Loan Repayment

Nurses working in critical shortage facilities may be eligible for forgiveness through the Nurse Corps Loan Repayment program. To qualify, you’ll need to:

Have attended a qualifying U.S. nursing school

Be either a registered nurse (RN), nurse faculty (NF), or advanced practice registered nurse (APRN)

Work full-time in a critical shortage facility or accredited nursing program

If you qualify, up to 85% of your nursing school debt can be forgiven.

Income-Driven Repayment Loan Forgiveness

Income-driven repayment (IDR) is a federal loan repayment option that bases your monthly loan payment on your income, rather than basing it on your remaining balance. If you make qualifying payments on an IDR plan for 20-25 years, your remaining loan balance can be forgiven.

Federal Direct Consolidation

If you’re struggling to manage several loan payments at once, consolidating may help you.

Federal Direct Consolidation loans allow you to combine multiple federal loans into one. Then, you’re given a new interest rate equal to the average of your initial interest rates, rounded to the nearest eighth of a percent.

While consolidating won’t save you on interest, it could provide you with access to more repayment options, such as a different repayment plan or a longer repayment period.

In some instances, consolidating may be necessary to qualify for certain forgiveness programs. If you have questions about how consolidating may impact your forgiveness opportunities, contact your loan servicer directly.

Private Student Loan Refinancing

If you don’t qualify for student loan forgiveness because you have private student loans, refinancing to a lower interest rate or a shorter repayment period may be your best bet.

A lower interest rate can reduce your monthly payment, as well as how much you pay over the life of the loan. A shorter repayment period will increase your monthly payment amount, but you’ll save on interest in the long run.

To qualify for a competitive refinance loan, you’ll need a stable income and a decent credit score. To explore your options for refinancing, complete the Sparrow application.

Final Thoughts from the Nest

If you’re confident you don’t qualify for President Biden’s student debt relief, don’t worry — there are other options you may qualify for. Start by verifying your eligibility for other student loan forgiveness programs. Then, decide whether consolidating or refinancing makes sense for you. If you’re unsure which route to take, contact your loan servicer for personalized recommendations.

Managing many student loan payments at once can be very difficult. That’s why student loan consolidation sounds so enticing. You can streamline your payments into one and make it easier on yourself. It sounds like the perfect solution. However, it’s essential to think about student loan consolidation pros and cons.

Before you start the application process, you should learn about the pros and cons of student loan consolidation so you can make the best decision possible. Lucky for you, this article is your guide to all things consolidation. Let’s get into it.

What is Student Loan Consolidation?

Student loan consolidation is the process of combining all your federal student loans into one. This is done through a Direct Consolidation Loan that you’ll apply for. A Direct Consolidation Loan is a form of Direct Loan offered by the government.

If you noticed that this sounds similar to student loan refinancing, you wouldn’t be the only one. Many people see consolidation and refinancing as the same thing. The reality, though, is that they’re pretty different. Here are a few differences.

You can only consolidate federal student loans. Meanwhile, you can refinance both federal and private student loans.

While an advantage of refinancing is the possibility of a lower interest rate, you probably won’t get that with consolidation. When you consolidate your loans, they will average all of your loan interest rates together and then round up to the nearest ⅛ percentage. This means it will most likely stay the same or go up.

When you consolidate, you’ll retain access to all of your federal benefits. Some loans, like the Federal Perkins Loans, need to be consolidated to access those benefits. Meanwhile, refinancing your federal loans would cause you to lose them.

Pros of Consolidating Student Loans

Simplifies Managing Your Debt

One advantage of student loan consolidation is it simplifies your debt payment. If you have multiple student loans, you understand how hard it can be to pay each one on time. By consolidating, you’ll only have one student loan instead of several. That way, you only worry about making a single payment per month.

Can Extend Your Repayment Term

When you consolidate, there is the possibility of getting an extended repayment plan. This extended plan can provide you the extra needed time to be able to pay off the loan. Plus, with an extended repayment, usually comes a lower monthly payment.

Can Lower Your Monthly Payment

As we mentioned, you might be able to lower your monthly payment when you consolidate. Typically, this will only happen if you get a longer loan term. This is because you’ll have more time to pay off the same amount of money, so you’ll pay less monthly.

For example, paying a $100 loan off in two months means making $50 monthly payments. If you extend the loan term to five months, then you’ll only pay $20 monthly. It’s the same concept with getting a longer loan term.

Cons of Consolidating Student Loans

You Could End Up Paying More

Unlike refinancing, you most likely won’t get an interest rate reduction through student loan consolidation. Your interest rate will either stay the same or go up. If you do get a higher interest rate, it would add to the overall cost of the loan and raise your monthly payments. So, you might have to pay more if you consolidate.

If You Consolidate Privately, You’ll Lose Federal Loan Benefits

When you consolidate privately, you will lose your federal benefits. This includes benefits like income-based repayment plans and loan forgiveness. So, you’ll want to think seriously about whether you’ll need these benefits or not. If you think you will, don’t consolidate privately.

You Could Pay More in Interest

As stated, when you consolidate, you could get a longer loan term. Although a longer term can be great, it does mean that you will pay more in the long run. Why? Because there will be more time for interest to build, and that interest will add to the overall cost.

For example, say you have a $30,000 loan with a 5% interest rate on a standard repayment plan of 10 years. Over those 10 years, you’ll pay an extra $8,184 in interest for a total of $38,184. If your loan term got extended to 20 years, then you’ll pay an extra $17,517 in interest for a total of $47,517.

FAQ About Consolidating Student Loans

Will consolidating my student loans hurt my credit?

No, Direct Consolidation Loans don’t have any kind of credit score requirement or even do a credit check. So, you don’t have to worry about anything popping up on your credit report. Your score will remain the same.

If you opt to refinance and consolidate privately, you will need to pass a credit check to qualify. This may temporarily hurt your credit score.

Does consolidating student loans lower your interest rate?

No, it does not. Your interest rate will most likely stay the same or go up. When determining your interest rate, the government takes the weighted average of all your loans’ interest rates and rounds it up.

Student loan consolidation and refinancing through a private lender, however, will likely get you a lower interest rate.

Is it better to consolidate or refinance student loans?

It depends on your situation since each has its pros and cons. Consolidating helps you better manage your debt, but you could end up spending more money. Refinancing can help you save a lot of money and manage your debt, but you would lose federal benefits. It’s really up to you and what your priorities are.

To help you make the decision, here’s a list of the top 4 refinance rates. Rather than searching for lenders one-by-one, we recommend starting the process with an automated student loan search tool. After you complete the free Sparrow application, we’ll show you the rates and terms you’d qualify for with 17+ premier lenders.

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

It’s a big decision to make, and student loan consolidation has its pros and cons. Be sure to take the time to think about it and figure out what’s best for you. That way, no matter what happens, at least you know you made the most well-informed decision.

If you choose to take a different route instead, like refinancing, use Sparrow to help you compare refinance rates across multiple lenders. The Sparrow application will match you with what you best qualify for from our partnering lenders. A lot of them offer great refinancing options. Plus, you’ll be able to refinance your federal and private loans together. To get started, fill out the Sparrow application.

According to an Education Data report, the average student loan debt is around $39,351 per borrower. As a result, it can be hard to make the average student loan monthly payment. If you’re currently experiencing this and are trying to figure out how you can cut costs, you’re in the right place.

Lucky for you, you can lower your monthly payments. How? Here is everything you need to know about monthly payments and how to lower them.

What is the Average Student Loan Monthly Payment?

According to the above report, the overall average student loan monthly payment is $460. This can change, however, depending on a variety of factors, such as degree type. Typically, the higher the degree, the more money you’ll owe. Yet, even within a degree, the average monthly payment can vary. Take a look at the table below to better understand.

Low Payment

Average Payment

High Payment

Associate’s Degree

$281

$333

$384

Bachelor’s Degree

$354

$448

$541

Master’s Degree

$350

$695

$1,039

Graduate Degree

$575

$1,210

$1,844

Professional Degree

$521

$1,537

$2,553

The reason these numbers vary is due to additional factors like salary and debt owed. Typically, people with larger salaries can afford to pay more. Similarly, the more debt you owe, the higher your repayment cost will be.

That’s why it’s important to understand these numbers. You can better understand how your financial situation influences your monthly payments. However, these factors (such as your degree type, salary, and debt owed) aren’t the only things impacting your payments.

How Your Interest Rate Impacts Your Monthly Payments

Interest rates determine the overall cost of borrowing a loan. They’re usually described as a percentage of the loan principal.

Interest rates can be pretty impactful. Education Data reports that about 67% of borrowers’ total cost of repayment is interest. It’s important, then, to get as low an interest rate as you can to keep those costs down.

For example, let’s say you took out a $30,000 loan with a 5% interest rate. You’re on a payment plan with a repayment period of 20 years. If you make only minimum monthly payments for the entire life of the loan, you’ll pay $47,517 with monthly payments of $198. But, look at what happens if we lower that interest rate to 4% and keep all other factors the same. Now, you’d pay $43,631 with a monthly payment of $182.

Loan 1

Loan 2

Balance

$30,000

$30,000

Interest Rate

5%

4%

Repayment Period

20 years

20 years

Monthly Payment

$198

$182

Total Cost

$45,517

$43,631

Notice how much money the lower interest rate saves you despite having the same repayment period and payment plan. Just that one percent decrease would save you $16/month, $192/ year, and around $2,000 over the course of the loan. As you can see, understanding your interest rate is extremely important. Especially on larger loan balances, or with higher interest rates, it can be the key to lowering your monthly payment significantly.

How to Lower Your Monthly Payment

Now that we better understand your monthly payments, let’s get into how you can lower them.

Refinance

By refinancing your student loan, you’re letting a private lender pay off your current loans. They’ll then give you a new private loan to cover what you owe them. You can get better terms on this new loan such as a lower interest rate. Thus, securing these new terms can lower your monthly payment and help you save money.

To qualify for refinancing, you’ll need to have a good credit score and steady income. Individual lenders may also have additional requirements you need to meet. Be sure to ask them about those before applying.

Rather than searching for refinance lenders one-by-one, we recommend starting the process with an automated student loan refinance search tool. With the free Sparrow application, you can see the rates and terms you’d qualify for with 17+ premier lenders.

Here is a list of the top refinance rates:

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

If you have multiple federal student loans, consolidating them can be a good idea. You’ll do this through a Direct Consolidation Loan. When you get a Direct Consolidation Loan, you’re combining all your federal loans into one. You’ll then only have one monthly payment to make as opposed to a few payments a month. Additionally, consolidating certain loans, like the Perkins Loan, makes them eligible for loan forgiveness.

It’s important to note that consolidating may not get you better terms like a lower interest rate. Still, it can simplify your monthly payments which, in turn, lowers how much you’ll pay per month.

To qualify, you must have loans in repayment or the 6-month grace period. If you’re currently still attending college, you cannot consolidate your loans yet.

Switch Repayment Plans

A more budget-friendly plan can lower your monthly payments. Federal borrowers, for example, have access to income-driven repayment (IDR) plans. These plans base your payments on your discretionary income. The idea is that by basing the payments on your annual income, it’ll help keep them more affordable for you.

Meanwhile, private loan borrowers can talk to their lenders to see if they offer similar plans. While these plans may not have as many benefits as an IDR plan, they can still save you money each month. Reach out to your lender if you have questions.

Pursue a Job with Debt Payoff Benefits

Imagine working for a company that offers to pay you extra money to put toward your student loans. It sounds like a dream, but it isn’t. Companies are already starting to offer debt payoff benefits, and many more are planning to add them in the future. That extra money they pay you means less money that you’ll have to pay for your monthly payments out of pocket.

Final Thoughts from the Nest

Your monthly student loan payment might be one of your biggest expenses. So, it’s worth knowing this information to help you better understand it and, hopefully, lower it. If you decide to lower your payment through refinancing, look no further than Sparrow.

Sparrow offers an application that will match you to what you best qualify for from our 15+ partnering lenders, many of which provide competitive refinancing offers. From there, you can compare the different lenders you’re interested in before making a final decision. Fill out the Sparrow application today to get one step closer to lowering your monthly payments.

When paying for college, a few thousand here and there might not seem like much. But overtime, it adds up quickly. And, with more expensive programs and advanced degrees, it’s hard to dodge the colossal tuition bills.

If you’re staring at a student loan balance of over $200,000, you might be feeling overwhelmed, and rightfully so. It may be challenging to conceptualize how one could possibly attack such a mountain of student loan debt.

The good news is this: It’s entirely possible, and we’re here to help you break it down. Here’s how to pay off $200,000 in student loans.

Student loan forgiveness programs can wipe out all, or some, of your student loan debt. That, combined with the very specific criteria of some programs, makes it a necessary starting point.

Oftentimes, student loan borrowers are unaware of such programs and their requirements, only learning about them when they are further along in their debt payoff journey. For example, the Public Service Loan Forgiveness program requires recipients to have made 120 qualifying monthly payments on an income-driven repayment plan. It is not uncommon for borrowers to have made payments for years without recognizing that they don’t count toward forgiveness as they weren’t on the proper repayment plan.

Thus, it’s important to consider these programs as soon as possible in your debt payoff journey. Making yourself aware of the options available can help you begin the process of meeting the necessary criteria before making non-qualifying payments.

Consider Refinancing Your Student Loans

If you have high-interest loans, refinancing should be your next step. Refinancing, in a simple sense, is the process of swapping your current loan(s) for one with a better interest rate or terms.