Typically, it’s recommended that borrowers have a good credit score to access competitive student loan offers. But what if you have no credit at all?

Don’t fret — there are a variety of student loan options for borrowers with no credit.

Keep reading to learn how you can get student loans with no credit and to explore our top picks for lenders.

Can You Get Student Loans if You Don’t Have Credit?

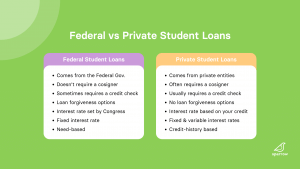

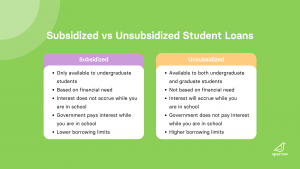

It depends on the type of loan you are borrowing. For federal loans, you do not need to have credit to qualify. On the flip side, most private student loans will require you to have a strong credit history.

However, there are still private loan options for those without a credit history. Borrowers can either apply for non-credit-based loan options or have a cosigner with a strong credit history cosign their loan. That said, borrowers should consider a cosigned loan option before non-cosigned, non-credit-based loans because the interest rates can be higher for the latter.

Student Loan Options if You Have No Credit

There are plenty of loan options available for prospective borrowers without any credit.

Federal Student Loans

Experts recommend that borrowers exhaust their federal loan options before resorting to private loans. Federal loans have controlled interest rates, strong borrower benefits, and variousrepayment plans, making them the preferred option.

Generally, most federal student loans have fixed interest rates that are set by Congress. This means that the interest rate on the loan will never change, protecting your interest rate from fluctuations due to the economy.

If you opt for private student loans, look into the lenders below. Rather than searching for lenders one-by-one, we recommend comparing your no credit options with an automated student loan search tool. With the free Sparrow application, you can see the rates and terms you’d qualify for with 17+ premier lenders.

Here are the best private student loans for no credit:

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

Ascent’s Non-Cosigned, Outcomes-Based loan is a great option for high school upperclassmen (including DACA recipients and international students) with limited credit/income and no cosigner. Qualifying students must have a GPA above 2.9.

Fixed interest rate: 13.09% to 15.08% Variable interest rate: 13.07% to 15.02%

Edly’s income-based repayment (IBR) loan is not like your average student loan. Students who are approved for an Edly IBR loan do not make payments during school but can make payments based on their income after graduation.

IBR loans are best for borrowers who want a loan that doesn’t require a cosigner or have a minimum credit score, in addition to flexible repayment plans and competitive repayment terms.

The APR on an IBR loan depends on your projected income, but the Edly IBR loan has a maximum 24% APR.

If you are a high-achieving undergraduate student with limited credit history and income, Funding U is the lender for you.

Funding U offers student loans without a cosigner, credit history, or income. Your eligibility as a borrower depends on your GPA and estimated future earnings.

Fixed interest rate: 7.49% to 12.99% Variable interest rate: Funding U does not offer variable interest rates.

MPOWER offers non-cosigned loans to domestic, international, and DACA undergraduate and graduate students. MPOWER is available in all 50 states and offers special discount rates for responsible borrowing.

Fixed interest rate: 13.74% (14.75% APR) Variable interest rate: MPOWER does not offer variable interest rates.

As a borrower, finding the best loan option for you is important for your future finances. As you sift through your options, be sure to compare loans across interest rates, repayment plans, and borrower protections.

Given the rising cost of college, finding affordable college financing is more important than ever. As a parent, it’s both understandable and admirable to want to support your child through the process of paying for college. It’s essential that you have the tools to pick the best college loan.

If you’re curious about your parent loan options, you’re in the right place. Here’s what you need to know to pick the best college loan for parents.

The best parent loan for you will ultimately be the one that suits your needs best. However, having a list of options that offer competitive interest rates, flexible repayment options, and strong customer service will make the search process easier.

The following are our top picks for the best private college loans for parents.

Parent Loans vs. Traditional Private Student Loans

While parent loans and traditional private student loans are similar in nature, there are some key differences you’ll want to consider before choosing one over the other.

A parent loan allows you to borrow on behalf of your child to finance their education. While you may require your child to make payments directly to you, you are legally the sole person responsible for paying back the loan.

A traditional student loan, however, is one that your child borrows on their own behalf. If you cosign the student loan, both you and your child are legally responsible for paying back the loan.

Both federal and private lenders offer parent loans. While similar in that parents can borrow both loan types on behalf of their child, they differ in several ways.

The only federal student loan parents can borrow on behalf of their child is the Parent PLUS Loan. To receive a Parent PLUS Loan, you must:

Be the biological or adoptive parent of a dependent undergraduate student who is enrolled at least half-time at an eligible school

Not have an adverse credit history

Meet the general requirements to receive federal student aid

The interest rate for Parent PLUS Loans is fixed and set by the government each year. For Parent PLUS Loans disbursed on or after July 1, 2022 and before July 1, 2023, the interest rate is 7.54%.

Like other federal student loans, Parent PLUS Loans have the opportunity to be forgiven, which is not available for private student loans. This is an important factor to consider if you plan to pursue any loan forgiveness programs.

Before borrowing a Parent PLUS Loan, you should check to see what rates you qualify for in private parent loans. You may find that some private lenders are able to offer you rates lower than the Parent PLUS Loan interest rate.

Private Parent Loans

Private parent loans are provided by private student loan lenders. Unlike federal Parent PLUS Loans, each individual private lender will offer different interest rates and terms. The eligibility criteria for private parent loans will vary, but in general, you must:

Meet income and/or credit requirements

Be borrowing on behalf of a student attending an eligible school

While it is commonly assumed that private student loans always have higher interest rates than federal student loans, that isn’t necessarily true. You should always compare both federal and private parent loan options before agreeing to one or the other.

Commonly Asked Questions About College Loans for Parents

What is the best way for parents to pay for college?

There is no single best way for parents to pay for their child’s college education. Generally speaking, however, you should begin by encouraging your child to pursue scholarship and grant opportunities. Both forms of aid do not need to be repaid.

Following that, consider what you’re able to contribute out-of-pocket. It’s important to minimize the amount you need to borrow.

After you’ve exhausted both options, consider both federal and private student loans.

Is it better to borrow a Parent PLUS Loan or a private parent loan?

One option isn’t necessarily better than the other. If you plan to pursue any loan forgiveness programs, you may prefer a Parent PLUS Loan over a private parent loan. If you are more concerned with finding a competitive interest rate, however, you may find that a private parent loan suits you better.

Do parents need good credit for student loans?

It depends on the lender. While most federal student loans do not factor your credit score into your eligibility, private student loans often do. That said, there are a variety of private student lenders that work with parent borrowers with lower credit scores.

To borrow private parent loans, see what rates you qualify for by completing the Sparrow application. In less than 3 minutes, we’ll show you which parent loans you qualify for and at what rates.

Final Thoughts from the Nest

There are a variety of parent loan options available, and while beneficial, it can make the process of picking the best option overwhelming. To simplify the process, start with Sparrow. Rather than searching endlessly for a parent loan that works for you, fill out the Sparrow application, and we’ll do the search for you. We’ll show you which parent loans you qualify for and at what rate so you can find the best option for you.

Sparrow’s goal is to give you the tools and confidence you need to improve your finances. Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. While we make an effort to include the best deals available to the general public, we make no warranty that such information represents all available products.

Some rates listed may include an Autopay Discount, which requires you to agree to make your monthly payments by an automatic monthly deduction (ACH) from a valid bank account. To verify whether the interest rates listed include an Autopay Discount, please read the individual lender disclosures.

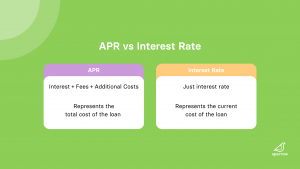

An important factor when shopping for student loans is looking at the interest rate. But interest rates can be a little confusing. You may ask yourself questions like:

What is a good interest rate?

How do they vary?

What should I even look for?

Before you panic, don’t worry. We’ve got your back. To give you an idea of what to look for in interest rates, let’s go over the average student loan interest rates.

Average Student Loan Interest Rate

Interest rates influence the total repayment costs you’ll have. So, to help you make a better-informed decision, it’s a good idea, then, to learn what interest rates are now. The interest rates will vary depending on a variety of factors. This includes what type of loan you get, your lender, and sometimes even your credit score.

For example, let’s take a look at the different federal student loan interest rates. These all vary depending on the type of loan and student. According to the federal student aid website, the current federal student loan interest rates are as follows:

Direct Unsubsidized Loans for Graduate or Professional Students – 6.54%

Direct PLUS Loans for Parents or Graduate/Professional Students – 7.54%

These interest rates are only applicable for the 2022-2023 school year. This includes any loans taken out on or after July 1, 2022, and before July 1, 2023.

Meanwhile, the average private student loan interest rate ranges from 6% to 7% according to Education Data. The exact interest rate you might get depends on your lender and financial situation. The overall average student loan interest rate, though, is 5.8%. This number includes data from both private and federal loans.

Student Loan Interest Rates on Sparrow

When shopping around for student loans, you want to look for the best interest rates. Sparrow partners with private lenders to get you those best rates. Here’s a quick overview of what interest rates you can find on Sparrow.

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

Keeping in mind that you’ll repay not only the loan principal but the interest also, a good student loan interest rate is going to be low. In general, the lower, the better. This is because the interest rate is an indicator of how much interest you’ll pay. The higher the interest rate, the more you can expect to pay during repayment. For example, let’s say you took out a $30,000 loan on a 15-year repayment term. Using that information, let’s create two scenarios with different interest rates.

In the first scenario, you’ll have an interest rate of 7%. With this interest rate, you’ll pay $48,537 over the course of your repayment period.

In scenario two, you’ll have an interest rate of 5.8%. With this interest rate, you’ll pay $44,987 throughout your repayment period.

Here’s a table to help you understand the information easier:

Scenario 1

Scenario 2

Loan Principal

$30,000

$30,000

Repayment Period

15 years

15 years

Interest Rate

7%

5.8%

Total Paid

$48,537

$44,987

Notice how even just a 1.2% difference in interest rates results in saving thousands of dollars. That’s why the best interest rates are the lowest rates you can get along with good repayment terms. Doing this will help you save a lot of money in the long run.

Final Thoughts from the Nest

Interest rates can be a little tricky. They vary a lot depending on the type of loan you have (or are looking for). The most important thing to keep in mind is to try to get as low an interest rate as you can with good loan terms.

As you saw earlier, Sparrow offers great interest rates from our partnering lenders. All you have to do to take advantage of these rates is fill out the Sparrow application. Once you do, it will match you with what you are qualified for from any of our 15+ partner lenders. So, get started now to find great private loans that best match what you need.

Sparrow aims to give you the tools and confidence you need to improve your finances. Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. While we make an effort to include the best deals available to the general public, we make no warranty that such information represents all available products.

Rates in this article were last updated on 11/07/2023. Rates may include an autopay discount and they are subject to change.

“Can I get a student loan even though I have bad credit?”

The simple answer: yes. The more complicated answer: welllll, yes, but it’s going to be trickier.

While most federal student loans don’t require you to have a good credit score, or any credit at all, most private student loans, on the other hand, do. If you’re worried about your poor credit score preventing you from being able to pay for college, don’t fret. While it may be more difficult, it isn’t entirely impossible.

Here’s what you can do to get a student loan with bad credit.

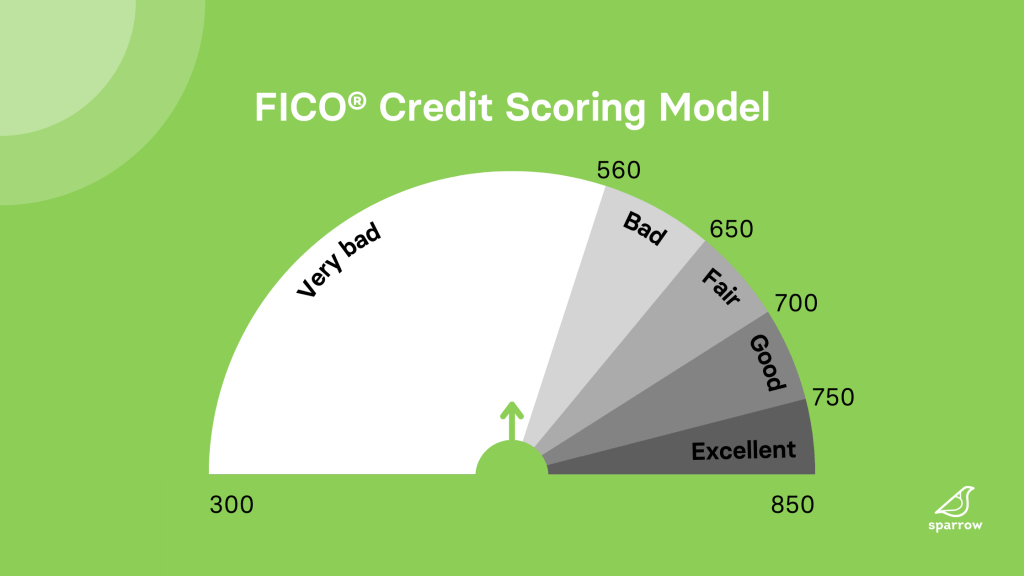

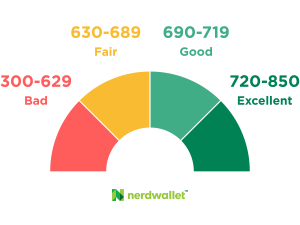

Generally speaking, you will need a credit score of at least 670 or higher to qualify with most private lenders. That said, what each individual lender considers “bad” credit will vary. And, there are several lenders that work with borrowers with lower credit scores.

It’s important to note that most private lenders use the FICO credit scoring model. The FICO scale uses a range of 300-850 to measure creditworthiness, so the closer you are to 850 the better.

First, here’s is a list of the top 5 student loans for bad credit. Rather than searching for lenders one-by-one, we recommend starting the process with an automated student loan search tool. After you complete the free Sparrow application, we’ll show you the rates and terms you’d qualify for with 17+ premier lenders.

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

The Arkansas Student Loan Authority (ASLA) is an Arkansas state entity that provides educational funding for all Arkansas students who wish to attend higher education institutions. ASLA has a minimum credit score requirement of 670. ASLA is a great option for Arkansas students.

Ascent is an online lender that offers educational funding for students. They offer three types of student loans: a traditional cosigned loan, a non-cosigned credit-based loan, and a non-cosigned outcomes-based loan. Collectively, the three options provide a great selection for those who do not have a cosigner available, are international or DACA students, or have lower credit scores. Ascent’s minimum credit requirement varies based on the loan.

Brazos is a non-profit lender offering educational funding through private student loans available only to Texas Residents. They offer a wide range of loan options, covering undergraduate, graduate, MBA, law, medical, dental, veterinary, and doctoral degree programs. Brazos does not disclose their minimum credit requirement. Brazos is a great option if you live in Texas and want competitive interest rates.

College Ave Student Loans offers educational funding for undergraduate, graduate, professional, and career school students, and parents of students. To qualify for a student loan with College Ave, you will need a credit score in the mid-600s. College Ave is a great option if you are seeking a more flexible repayment term that allows you to find a loan that matches your budget.

Earnest’s student loans provide funding to undergraduate, graduate, and professional students. Earnest has a minimum credit score requirement of 650. They’re a great option if you are seeking competitive interest rates, unique borrower perks, and flexible repayment options that allow you to find a loan that matches your budget.

Edly Income-Based Repayment (IBR) Student Loans, originated by Edly’s partner FinWise Bank, provide an alternative loan option for students. Students who are approved for an Edly student loan will not have to make payments while in school. Instead, borrowers make payments after graduation based on their income. Due to the structure of IBR loans, borrowers have a variety of benefits when it comes to repayment. An Edly IBR loan is best if you are seeking a loan option with no cosigner, competitive repayment terms, and flexible repayment options.

Funding U is an online lender that focuses exclusively on undergraduate students with no cosigner. Rather than looking at your credit score or income, Funding U looks at non-traditional metrics such as your school, major, GPA and estimated future earnings to assess your creditworthiness. Funding U’s student loan is best if you are a high-achieving undergraduate student with limited credit history and no access to a creditworthy cosigner.

LendKey is an institution that offers educational funding to undergraduate and graduate students. By connecting borrowers with a network of 100+ lesser-known credit unions and community banks, LendKey allows you to work with smaller lenders with low rates and good customer service, rather than traditional lending institutions. LendKey has a minimum credit requirement of 660. It’s best for students who want generous cosigner release and forbearance policies.

MPOWER is an online lender that offers educational funding to international, domestic, and DACA students. They offer non-cosigned undergraduate and graduate student loans. It is best for international students and DACA students who don’t have a credit history and can’t access a qualified cosigner.

Can You Get Federal Student Loans with Bad Credit?

Most federal student loans don’t require you to have a good credit score (or any credit at all). They also tend to have lower interest rates and better terms and conditions. These qualities make them a great place to start when thinking about financing your college education.

There are four main types of federal student loans, three of which do not require a credit check or a high credit score to qualify.

Federal Loans that Don’t Require a Credit Check

Direct Subsidized Loans

Direct Subsidized Loans are available only to undergraduate students who demonstrate financial need. This means that you may not qualify for Direct Subsidized Loans.

If you do, the government will pay the interest on your Direct Subsidized Loans while you are in school. Once you graduate, you’ll be in charge of paying them back, interest included.

Direct Unsubsidized Loans

Direct Unsubsidized Loans are available to both undergraduate and graduate students, and you do not need to prove financial need to qualify. However, while in school, the government does not pay interest on these loans. So, while you’re hitting the books, interest will be accumulating in the meantime.

Direct Consolidation Loans

Direct Consolidation Loans allow you to combine more than one federal loan into one. So, if you have several federal loans and want to simplify your payments, you can combine them into one singular loan, and thus, one singular payment. When you consolidate, your new interest rate is the average of your previous loans’ interest rates.

Federal Loans That Do Require a Credit Check

Direct PLUS Loans

Direct PLUS Loans are available to graduate/professional students and parents of students. Like Unsubsidized Loans, you will be responsible for any interest that accrues, even while in school. However, unlike all other federal loan types, Direct PLUS Loansdo require an adverse credit check.

While the credit check process could be a bummer if you have bad credit, there is hope if you don’t pass it. Adding a creditworthy endorser to the loan may allow you to qualify.

How to Get Federal Loans with Bad Credit

In order to get federal aid, you need to fill out the Free Application for Federal Student Aid (FAFSA). This form will ask you to provide information regarding you and your family’s financial situation to determine your eligibility for aid, but it will not run a credit check as part of that evaluation.

It’s important to note that you don’t have to accept all the federal aid that you qualify for. You should always consider the terms and conditions and think about what makes most sense for you and your educational journey.

While federal loans do tend to be a better choice in comparison to private student loans, they won’t always be best. There’s a variety of different financial aid options for students, so make sure you understand what they all are and what they all mean before agreeing to one.

The goal of student loan refinancing is typically to score a lower interest rate or monthly payment, saving you money in the long run. If you have a bad credit score, it may be challenging to secure a lower rate than what you currently have.

Here is a list of the top refinance loan companies for bad credit. In just three minutes, you can compare real and personalized student loan refinancing rates from 17+ lenders – for free – by using the Sparrow application.

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

The Arkansas Student Loan Authority (ASLA) is an Arkansas state entity that provides student loan refinancing for Arkansas residents. ASLA has a minimum credit score requirement of 670.

College Ave offers student loan refinancing with competitive rates, flexible repayment terms, and strong customer service. Their student loan refinance offering is best if you are seeking a more flexible repayment term that allows you to find a loan that matches your budget. To qualify for a refinance loan with College Ave, you will need a credit score in the mid-600s.

LendKey is an institution that offers educational funding to undergraduate and graduate students. By connecting borrowers with a network of 100+ lesser-known credit unions and community banks, LendKey allows you to work with smaller lenders with low rates and good customer service, rather than traditional lending institutions. LendKey has a minimum credit requirement of 660. It’s best for students who want generous cosigner release and forbearance policies.

Earnest’s student loans provide funding to undergraduate, graduate, and professional students. Earnest has a minimum credit score requirement of 650. They’re a great option if you are seeking competitive interest rates, unique borrower perks, and flexible repayment options that allow you to find a loan that matches your budget.

ISL is a nonprofit lender that offers both private student loans and student loan refinancing. ISL’s student loan refinancing is best if you haven’t graduated and want generous forbearance policies. ISL has a minimum credit score of 670.

SoFi is one of the largest student loan refinance companies in the industry. With competitive interest rates, a diverse set of repayment options, and exclusive member benefits, SoFi is a good fit for borrowers with an associate’s degree or higher or borrowers with a high income. SoFi has a minimum credit score of 650.

What to Do if You Were Denied a Student Loan Due to Bad Credit

If you were initially denied a private student loan due to poor credit, your best bet is to look for a creditworthy cosigner. A cosigner is someone who agrees to sign onto the loan. In doing so, they agree that if the borrower fails to repay the loan, the cosigner will take responsibility for paying it back.

Having a cosigner is valuable because their credit score will be factored into the lender’s decision to work with you, which can also help you secure a better interest rate and terms. So, if your credit score isn’t up to par but theirs is, you may be in luck.

Make sure you don’t pick just anyone to cosign unless you really, really have to. Make sure to find someone that is creditworthy and has a history of managing their finances effectively. Additionally, always make sure to have open conversations with whoever you choose before they agree to cosign. Explain the pros and cons of being a cosigner and what impact it could have for them. Discussing expectations around repaying the loan is also important so your cosigner knows what to expect.

Improving your credit score won’t happen overnight, but it is worthwhile to take any steps you can throughout the loan process to boost your credit.

Here’s a few tips to help get your credit score in check.

Stay Aware of How Much Debt You’re Taking On

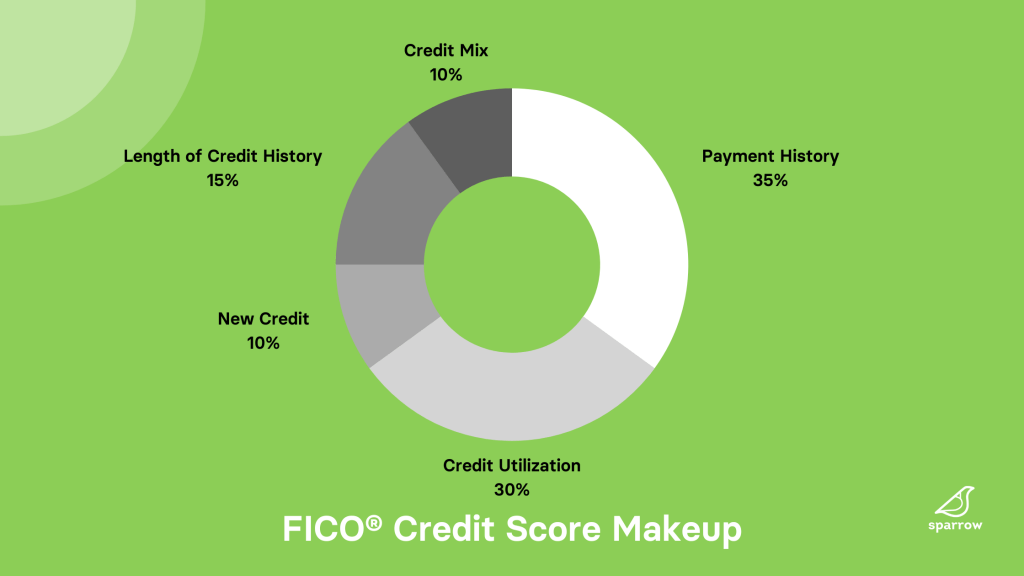

Your credit score is calculated based on a variety of factors, one being your payment history. In fact, your payment history is the most important part of your credit score, making up 35% of the calculation.

When you take on debt, such as student loans, you are doing so with the understanding that that money will be paid back and paid on time. If you make consistent, on-time payments, it’s good for your credit, as it demonstrates an ability to pay back debts successfully. If you pay late or miss payments, it could hurt your credit, as it demonstrates an inability to pay back debts successfully.

While this may sound like a no-brainer, you’ll want to be aware of how much debt you’re taking on. If you take on too much, it could make you more likely to miss a payment or go into loan default.

Remember to be realistic about how much you will be able to afford in monthly payments. Utilizing a student loan calculator to estimate your monthly loan payments after graduation is a great way to get real about whether the loan will be feasible when repayment starts. Let’s use an example here.

Let’s say you’re studying to be a public school teacher, and you land a job making $50,000 a year after graduation. This would land you around $4,200 per month (if we round up) to budget with. (For the ease of this example, we aren’t factoring in taxes.)

Now, let’s say your monthly expenses are as follows:

You’re left with $1,950 each month. This example is simple and doesn’t factor in taxes or other expenses such as savings, car maintenance, pet costs, entertainment, and more.

If you’re debating a $30,000 student loan at a 9% interest rate and a 15-year repayment term, you’d be looking at a $304 minimum monthly payment. Now remember, this is for one loan. If you took out four of these loans, one for each year you’re in school, you’re looking at an even heftier monthly payment.

So, before taking out a student loan, consider whether the estimated monthly payments would be affordable for you given your future income potential. Being realistic about what you may be able to afford could prevent you from missing a payment down the line.

The length of your credit history is another important factor in determining your credit score. The longer you have had open lines of credit, the better your credit score will typically be. Having, and properly managing, your credit for a long time shows lenders that you’re responsible.

While it may sound counterintuitive, closing any open lines of credit you currently have could hurt your credit score because it shortens the length of your credit history. Unless you absolutely need to, stay away from closing any current accounts.

Don’t Open New Lines of Credit

Opening new lines of credit will cause what’s called a hard inquiry. A hard inquiry occurs when a financial institution checks your credit report before making a lending decision. When lenders do a hard inquiry, they’re attempting to assess how you’ve handled your credit in the past.

Just like you’d only lend money to someone you trust, lenders want to make sure you’re a sound investment for them before dishing out the cash. A hard inquiry, though, can temporarily hurt your credit. So, if you’re looking to take out a student loan anytime soon, we recommend holding off on opening any new lines of credit.

Check Your Credit Report

If you have bad credit but aren’t totally sure why, you may want to check your credit report. Your credit report is important to look over for many reasons, but especially to check for errors, fraud, or identity theft. Even a small error on your credit report can significantly hurt your credit score, so we recommend checking fairly often.

There are many financial institutions, such as banks and credit card companies, that offer free credit reports. If yours don’t, utilize the free Annual Credit Report website. You are, by law, entitled to these reports yearly.

Final Thoughts from the Nest

So, yes. You can get a student loan with bad credit. However, it might make the process a bit more challenging. Start thinking ahead about where your credit is at, and if it’s not ideal, start taking small steps to build it. To find a private student loan for students with bad/no credit, complete the Sparrow application today.

Sparrow’s goal is to give you the tools and confidence you need to improve your finances. Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. While we make an effort to include the best deals available to the general public, we make no warranty that such information represents all available products.

While an important piece in determining your eligibility for financial aid, Expected Family Contribution, or EFC, is often misunderstood.

Here’s what you need to know about Expected Family Contribution for FAFSA purposes.

What is Expected Family Contribution?

Expected Family Contribution, or EFC, is a number used to determine how much financial aid you are eligible to receive, including grants and federal student loans.

EFC is calculated using a formula established by law. The formula uses information such as:

Your/Your family’s income

Your/Your family’s assets

Your/Your family’s benefits

The number of family members in college during the same year

This information is then used to estimate the amount of money you and your family would be able to contribute to one year of college costs. By doing so, financial aid programs are able to estimate what your financial need may be when it comes to paying for college.

Note that this number does not indicate how much you will receive in financial aid or how much you willhave to contribute, but rather, how much you are eligible to receive and how much you could contribute.

Your EFC is important because it contributes to how you are evaluated for financial aid overall, including federal student aid.

Expected Family Contribution and Federal Student Aid

When calculating your overall federal student aid eligibility, the federal government uses a formula that takes into account several factors such as:

Your EFC

Student enrollment status (full-time, part-time, etc)

Your year in school

The cost of attendance each respective school

Federal student aid haslimits, and thus, your overall federal student aid eligibility helps determine how much of each type of aid you are eligible for.

How Does My Expected Family Contribution Impact My Federal Aid?

Your EFC will help determine how much aid you will be eligible for. If your EFC is $0, you will be eligible to receive the maximum amount of federal aid. If your EFC is over a certain threshold, you will receive no aid at all.

Note that these numbers may fluctuate annually to reflect changes in your/your family’s income.

Your Expected Family Contribution’s Impact on Financial Aid Overall

Each piece of this overall aid eligibility equation helps paint a bigger picture regarding your finances, and therefore, helps schools understand where you may need financial aid.

How much of your financial need is covered by federal aid may impact how schools fill the remaining gap with aid such as university scholarships and grants.

Why Your Expected Family Contribution Changes

Your EFC will likely change year-to-year as you or your parent’s/parents’ income changes. Therefore, the amount of aid you are eligible for each year will also change.

Be sure to resubmit your FAFSA each year to ensure that you maintain access to the maximum amount of aid you are able to receive.

How Can I Calculate My Expected Family Contribution?

Let us say this before we give you the breakdown: While you can calculate your own EFC at home, be careful not to get overly attached to this number. At-home estimates are just that: estimates.

Add up the total parent income (both taxed and untaxed income)

Subtract allowances for federal and state taxes, as well as any Social Security paid

Subtract an Income Protection Allowance (IPA)

This number is intended to estimate how much a family would need for necessities such as housing and food based on its size. This number would be taken out of the overall income when calculating how much a parent would be able to contribute to a child’s education.

Subtract an Employment Expense Allowance

This will only apply for households where all parents are working, and will equal 35% of earned income or $4,000 — whichever is less. This amount is intended to cover the expenses that working parents have such as commuting.

After doing this calculation, you will reach what’s called your Available Income (AI). This represents how much of the parental income can be considered for college costs.

Calculating the Student Contribution to the EFC

Add up the total student income

Subtract allowances for federal and state taxes, as well as any Social Security paid

Subtract an IPA

Figure out the Student Contribution from Available Income (50% of the current total)

Finally, add the Parental Contribution to the Student Contribution to result in your family’s EFC.

Commonly Asked Questions About Expected Family Contribution

What is the Expected Family Contribution for an independent student?

When you are a dependent student, your EFC is calculated based on both your parent’s/parents’ income and your own.

However, as an independent student, your family’s income will not be used to calculate your EFC. Rather, your own income and assets will be factored into the calculation, minus some deductions.

If you are an independent without dependents, your EFC will be based on your income (and your spouse’s if you are married) minus taxes and basic living expenses.

If you are an independent with dependents, your EFC will be based on your income (and your spouse’s if you are married) minus taxes, basic living expenses, and an employment allowance. The employment allowance is available if you are a single working parent or a working student with a spouse.

There is no one specific number that makes your EFC “good.” Generally speaking, however, the lower your EFC, the more financial aid you may qualify for.

Why is my Expected Family Contribution so high?

Your EFC can be high for a variety of reasons, however, it is often high due to having a high income or a lot of assets. Assets are resources that can produce positive economic value such as:

Cash

Real estate

Stock holdings

When calculating your EFC, both liquid and illiquid assets are taken into account. Liquid assets are ones that can be sold quickly without losing a lot of their value, such as the money in your bank account or stocks. Illiquid assets, on the other hand, are ones that do lose value when sold quickly, such as cars and real estate.

If you/your family has a low income but a lot of assets, your EFC may be higher than you expected. If this does not seem to be the case, however, consider filing a financial aid appeal to have your EFC recalculated.

Your EFC is one piece of how your financial aid eligibility is calculated. While it isn’t the whole bit, it is important. By estimating your family’s EFC, you can determine what financial gaps may arise after receiving financial aid.

If scholarships and federal student aid don’t cover your financial need completely, it may be time to explore a student loan to fill the gap. When you’re ready, Sparrow is here to help.

Earning a graduate degree is a great way to increase your income potential. In fact, Indeed reported that, on average, the earnings increase from a bachelor’s to master’s degree is roughly 20%. Nonetheless, it can be difficult to understand how to pay for grad school.

Graduate school can be expensive. According to FinAid.org, a graduate degree costs anywhere from $30,000 to $120,000, depending on the program. This makes financial decisions around paying for graduate school even more important.

While that reality may be overwhelming, there are several ways to pay for your graduate degree. Let’s break down your top 5 options: scholarships, fellowships, grants, work-study, and loans.

How To Pay for Grad School

As with any degree, there is a certain order you should follow when it comes to how you finance your education.

Scholarships, fellowships, and grants are all forms of free aid, or gift aid. Typically, scholarships, fellowships, and grants do not need to be paid back, so you’ll want to accept these first.

After accepting any free money available to you, you should pursue work-study next. Federal work-study is considered earned money, meaning you have to trade your time to receive it. While not everyone will receive federal work-study, it’s a great option for those who do.

Loans should always come last in the process because they are borrowed money. When you borrow a loan, it’ll typically accrue interest, and by the time you pay it back, you’ll have paid a significant amount in interest.

#1: Finding the Best Scholarships for Graduate School

Graduate scholarships are typically awarded based on academic or professional achievements. However, there are scholarships awarded based on other factors such as:

What GPA Do You Need to Get Graduate School Scholarships?

Typically, you’ll need around a 3.5 GPA to be a competitive applicant for most graduate school scholarships. That said, there are scholarship programs that have a lower GPA minimum.

Where Can You Find Graduate School Scholarships?

You can find graduate school scholarships in a variety of places such as:

Professional organizations

From your school’s financial aid office

Online search engines

For example, the American Bar Association offers scholarships to first-year law students from underrepresented communities through theirLegal Opportunity Scholarship.

For search engines, there are a wide variety of options available such as ScholarshipOwl, Scholarships.com, Chegg, and Fastweb.

#2: Exploring Graduate Fellowship Options

A fellowship is another form of free aid that you’ll want to seek out before taking on student loans.

What is a Graduate Fellowship?

A fellowship is an award given to graduate students to subsidize the cost of education. Some fellowships are awarded simply to fund your education, similar to scholarships. Other fellowships are awarded specifically to fund academic projects such as dissertations, thesis projects, or research.

Fellowships are awarded by schools, professional organizations, and nonprofits, typically based on merit.

The amount you receive from a fellowship depends on the specific program. For example, the NSF Graduate Research Fellowship Program is a five-year fellowship that provides three years of financial support. Recipients receive an annual stipend of $34,000 and a cost of education allowance of $12,000.

The International Dissertation Research Fellowship (IDRF), however, provides a one-time stipend that varies depending on the research plan of the recipient. On average, each IDRF recipient receives $23,000.

When searching for a graduate fellowship, pay close attention to the length of the program and how the funds are disbursed to you or your university.

Is a Fellowship Better Than a Scholarship?

Fellowships and scholarships are both forms of free money, but you may have to complete an academic project to receive fellowship funding. If you’re interested in a particular academic project, a fellowship may be a solid option for you. If you’d prefer to receive free money with no strings attached, a traditional scholarship may be better for you.

While one is not necessarily better than the other, it’s important to understand how each one works to make an educated decision.

#3: Finding the Best Grants for Graduate School

Grants are similar to both scholarships and fellowships — they are free money you don’t need to pay back.

Who is Eligible for a Grant for Graduate School?

Typically, grants are awarded based on financial need. Some grant providers may have additional eligibility requirements such as having a certain GPA or enrollment in a specific program. Some may even require you to have specific research goals.

Graduate school grants can come from a variety of sources such as the federal and state government, your school, and professional organizations.

Federal Grants

To be eligible for any federal grants, you must complete the FAFSA. The information you provide on the FAFSA is used to determine your financial need, which is then used to determine your federal grant eligibility.

Does the Pell Grant Cover Graduate School?

As a graduate student, you are not eligible for the Pell Grant. The Pell Grant is intended for undergraduate students, minus a few exceptions.

State Grants

State grants are provided by individual U.S. states, and thus, each state grant program runs a little differently. Reach out to your state’s department of education to learn more about the grants they may offer.

School Grants

Some universities offer grants to students pursuing a graduate degree at their institution. Check with your specific program to learn more about the grants offered for your field of study. Don’t hesitate to ask the school’s financial aid office as well. There may be generic institutional grants available to both undergraduate and graduate students that you qualify for.

Professional Organization Grants

Professional organizations focus on advancing individuals within a particular profession or with specific interests. Because of this, they tend to offer financial assistance to those pursuing degrees within their field. For example, the American Bar Association and the American Marketing Association provide grants to eligible individuals pursuing related degrees.

Work-study is a federal aid program that provides part-time jobs to undergraduate and graduate students with financial need. To be eligible for work-study, you must complete the FAFSA. Your application will determine if your level of financial need meets the minimum requirement of the work-study program.

Both full-time and part-time graduate students are eligible for work-study. If you accept the work-study aid offered to you, you will be responsible for finding a work-study role through your college/university. Speak to your school’s financial aid office for specific information regarding how work-study functions at your school.

How Much Money Can You Get in Work-Study?

The exact amount you receive in work-study will depend on the school you attend. Although, at minimum, work-study roles must pay the federal minimum wage. However, there are some work-study roles that offer more generous hourly rates.

#5: Finding the Best Student Loans for Graduate School

Student loans should always be the last option when determining how to pay for grad school. The more you borrow, the more you will have to pay back due to the interest that accrues. That makes selecting a good student loan that much more important.

A cosigner is an individual that signs onto a loan alongside you, taking full responsibility for the loan if you’re unable to pay it back. A creditworthy cosigner can help you secure a lower interest rate and better terms.

If you don’t have access to a cosigner, that is okay, too. Non-cosigned loan options are available, but they may have higher interest rates.

If you are pursuing a graduate degree immediately after your undergraduate degree, you may not have a substantial full-time income just yet. Some private lenders have minimum income requirements, so if you plan to take out the loan without a cosigner, you’ll need to make sure you meet that income threshold.

Interest Rate

Each student loan will have its own unique interest rate and terms. Always compare interest rates carefully to select the loan that is best for you.

Each individual lender will offer a unique set of repayment options. While some lenders may offer a deferred repayment option, allowing you to postpone repayment while in school, others may only offer immediate repayment. This would force you to begin making loan payments while in school, which many students are unable to do. Be realistic about which repayment options would work for you and ensure the lender you select offers them.

Federal & Private Loan Options for Graduate School

As a graduate student, you will likely have access to both federal and private student loans.

Federal

Federal student loans are provided by the federal government. To be eligible for a federal student loan, you must complete the FAFSA.

Private

Private student loans are provided by private entities such as banks, financial institutions, and nonprofits. To see what private student loans you qualify for, complete the Sparrow application.

The Arkansas Student Loan Authority (ASLA) is an Arkansas state entity that provides educational funding for all Arkansas students who wish to attend higher education institutions. ASLA is a great option for Arkansas students.

Ascent is an online lender that offers three types of student loans: a traditional cosigned loan, a non-cosigned credit-based loan, and a non-cosigned outcomes-based loan. Collectively, the three options provide a great selection for those who do not have a cosigner available, are international or DACA students, or have lower credit scores.

Brazos is a non-profit lender offering private student loans to Texas Residents. They offer a wide range of loan options, covering undergraduate, graduate, MBA, law, medical, dental, veterinary, and doctoral degree programs. Therefore, Brazos is a great option if you live in Texas, have strong credit, and want competitive interest rates.

College Ave’s student loan offering is available for undergraduate, graduate, professional, and career school students, as well as parents of students. Accordingly, it’s best if you are seeking a more flexible repayment term that allows you to find a loan that matches your budget.

Earnest’s student loans are available to undergraduate, graduate, and professional students. It is best if you are seeking competitive interest rates, unique borrower perks, and flexible repayment options that allow you to find a loan that matches your budget.

By connecting borrowers with a network of 100+ lesser-known credit unions and community banks, LendKey allows you to work with smaller lenders with low rates and good customer service, rather than traditional lending institutions. LendKey’s student loan offering is available to undergraduate and graduate students. In addition, it’s best if you have strong credit and want generous cosigner release and forbearance policies.

MPOWER is an online lender that offers non-cosigned undergraduate and graduate student loans to international, domestic, and DACA students. Accordingly, it is best for international students and DACA students who don’t have a credit history and can’t access a qualified cosigner.

Prodigy Finance is an online lender that offers non-cosigned graduate student loans to international students. Accordingly, it is best for international students who don’t have a credit history and can’t access a qualified cosigner.

SoFi is a strong option for undergraduate, graduate, law, and MBA students, as well as parents looking to fund their child’s education. With competitive interest rates, a diverse set of repayment options, and exclusive member benefits, SoFi is a good fit for borrowers with a strong credit score or a creditworthy cosigner.

Final Thoughts from the Nest

While graduate school can be a costly affair, there are a variety of ways to pay for it. When figuring out how to pay for grad school, always remember to pursue aid in the following order: scholarships, grants, fellowships, work-study, student loans.

When it comes time to check out private student loan options, start with Sparrow.

Sparrow’s goal is to give you the tools and confidence you need to improve your finances. Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. While we make an effort to include the best deals available to the general public, we make no warranty that such information represents all available products.

If you’re a borrower, you may be wondering, “Are student loan payments tax deductible?”

For qualifying borrowers, the answer is yes. Student loan payments ARE tax deductible. The student loan interest deduction is a federal tax break that lowers how much of your income is taxed. The federal government created this deduction to assist borrowers in paying for higher education.

To find out if you’re eligible for this tax deduction, keep reading.

What Is The Student Loan Interest Deduction?

The student loan interest deduction is a federal income tax deduction that allows qualifying borrowers to deduct up to $2,500 from their taxable income.

Your eligibility for this deduction depends on your filing status and income level.

How Does the Student Loan Tax Deduction Work?

The student loan tax deduction enables you to subtract up to $2,500 from your taxable income for the interest paid on your student loans. Accordingly, this deduction helps you pay less in federal taxes. The Internal Revenue Service (IRS), the federal tax collection agency, offers various tax deductions, including student loan interest deduction.

To receive the deduction, you need to claim an “adjustment to income” on a 1040 form. Fortunately, you do not have to fill out a Schedule A, which is used for itemized deductions. To make this process as quick and easy as possible, gather the following information:

Filing status

Basic income information

Your adjusted gross income

Educational expenses paid with nontaxable funds

If you paid more than $600 in interest on your student loan debt, your lender/loan provider will give you a 1098-E.

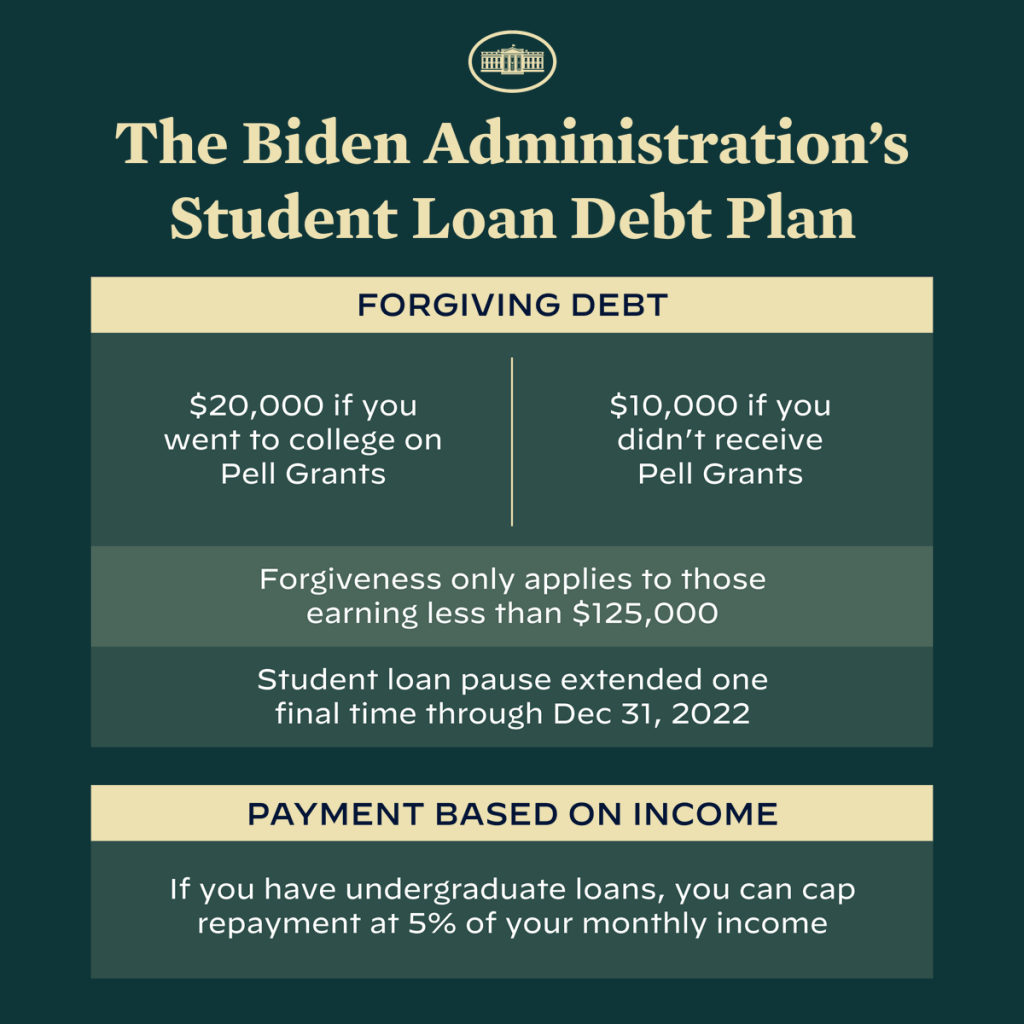

Note: The deduction applies only to non-federal loans that gathered interest, as the Biden administration placed federal student loans in forbearance in 2021. Learn more about Biden’s student loan forgiveness.

Who Qualifies for the Student Loan Tax Deduction?

To qualify for the student loan tax deduction, you must meet the following eligibility requirements in income, filing status, loan timeline, and loan type.

Income Your modified adjusted gross income (MAGI) is your income after subtracting applicable tax penalties and tax deductions. While you can calculate your MAGI manually, online calculators can simplify the process.

If you are a single filer, your MAGI must be less than $85,000 to qualify for the student loan tax deduction.

If you are a joint filer, your MAGI must be less than $170,000 to qualify.

Filing Status To claim the student loan tax deduction, the eligible loan must have been borrowed for one of the following:

You are claimed as a dependent on someone else’s tax return.

You borrowed the student loan in your name but your parents are making the loan payments.

You are a parent paying for the loan taken out in your child’s name, as you are not the legal owner of the loan.

Loan Timeline The student loan must have been taken out during an academic period when you were enrolled for at least half the time at a qualifying post-secondary institution.

Additionally, it must have been used during a reasonable period after it was taken out, with loan amounts used within 90 days of the academic period.

The latest rates from Sparrow’s partners

See a rate you like? Click Apply and we’ll take you to the right place to get started with the lender of your choosing.

Compare your personalized, pre-qualified rates from these lenders in minutes.

Loan Type Both federal and private student loans qualify for this deduction. However, you must have paid interest for the loan in 2019, as the student loan interest deduction was introduced in the 2020 Coronavirus Tax Relief.

Note: You can claim prepaid loan interest and origination fees for the student loan tax deduction.

Is It Worth Claiming Student Loan Interest on Taxes?

Regardless of your income class, you should claim your student loan interest on taxes if you qualify. Claiming this deduction will not result in any loss, as it lowers your taxable income.

How Much Can You Save with the Student Loan Interest Deduction?

The amount of money you can save depends on your income. The following table shows the average deduction values you can expect, based on your income class.

Income Class

Deduction Value

Below $10,000

$214

$10,000 to $20,000

$89

$20,000 to $30,000

$136

$30,000 to $40,000

$142

$40,000 to $50,000

$155

$50,000 to $75,000

$213

$75,000 to $100,000

$183

$100,000 to $200,000

$214

$200,000 and over

$74

Closing Thoughts From the Nest

If you qualify for the student loan interest deduction, be sure to claim the adjustment on your 1040 tax form. Doing so will reduce your taxable income. Accordingly, it will reduce the amount of taxes you owe.

With President Biden’s student loan forgiveness program dominating news headlines as the federal courts debate the legality of his debt relief plan, you may be wondering, “What is student loan forgiveness?”

If that’s the case for you, you’re in the right place. Keep reading to learn about what student loan forgiveness is and what programs you might qualify for.

How Student Loan Forgiveness Works

Student loan forgiveness wipes out all or part of your remaining student loan balance for federal loans only. However, there are strict eligibility requirements to qualify for federal student loan forgiveness. In fact, most debt relief are only offered for public service occupations.

Student Loan Forgiveness Programs to Consider

Public Service Loan Forgiveness

Public Service Loan Forgiveness (PSLF) is a program that offers debt relief for qualifying individuals who work in public service, whether that be volunteer work, medical practice, or other public sector work.

To qualify for Public Service Loan Forgiveness, you must :

Have paid the minimum amount due on time for 120 payments (10 years total).

Have worked 10 years in a public sector role.

Have borrowed Direct Loans or consolidated their federal loans into Direct Loans.

Loan Forgiveness Through Repayment Plans

Certain federal repayment plans offer loan forgiveness if enough qualifying payments are made on the loan. While this may take substantially longer than federal loan forgiveness programs, borrowers will still be able to receive debt relief.

Income-Based Repayment

Income-based repayment (IBR) is a repayment plan where the maximum monthly payments are between 10% to 15% of your discretionary income.

You must have 20-25 years of qualifying payments under your belt to be eligible for loan forgiveness.

Income-Contingent Repayment

Income-contingent repayment (ICR) is a repayment plan that is (hence the name) contingent on your income. Your monthly payments are recalculated every year based on your family size, outstanding loan balance, and gross income. Generally, your monthly payments will be around 20% of your discretionary income.

You must have 25 years of qualifying payments to be eligible for loan forgiveness.

Pay As You Earn (PAYE)

Pay As You Earn (PAYE) is a repayment plan where your monthly payments are 10% of your discretionary income and capped at how much you would pay on a regular, 10-year repayment plan.

The main benefit of the PAYE repayment plan, however, is that the government will pay 100% of the unpaid interest on your subsidized loans for the first three years.

To qualify for PAYE, you must demonstrate financial hardship and have received a federal loan after October 1, 2007. You must then make 20 years of qualifying payments to be eligible for forgiveness.

Revised Pay As You Earn (REPAYE)

REPAYE is the revised version of PAYE that has slightly different terms. The monthly payments for the REPAYE plan are 10% of your discretionary income with no cap, meaning that you could be paying more than you would on a standard 10-year plan.

With this plan, the federal government will:

Pay 100% of the unpaid interest on your subsidized loans for the first three years; or

Pay 50% of the unpaid interest on your subsidized loans and unsubsidized loans after the first three years.

Anyone with federal loans can be eligible for the REPAYE plan. You must then make 20 years of qualifying payments to be eligible for debt relief for undergraduate loans, or 25 years of qualifying payments for graduate loans.

Specialized Loan Forgiveness

If you have a specialized career, you may be eligible for loan forgiveness programs, such as:

Army National Guard Student Loan Repayment Program: If you’re a member of the Army National Guard you may qualify to have $50,000 shaved off of your federal loans. You must have Direct, Perkins, or Stafford loans.

Teacher Loan Forgiveness Program: If you are a full-time teacher who works in a low-income school or other eligible educational agency, you may be eligible for $5,000 to $17,500 in loan forgiveness. You must have worked full-time for a qualifying position for five consecutive years, and have Direct or Stafford loans.

Segal AmeriCorps Education Award: If you were a part of the AmeriCorps VISTA, AmeriCorps State, or AmeriCorps NCCC, you may be eligible to receive up to the maximum Pell Grant award to pay off your federal student loans.

Borrower Defense

If your school significantly deceived, defrauded, or scammed you, you may be eligible for borrower defense to loan payment forgiveness.

If you qualify for borrower defense, you will receive loan discharge. Loan discharge, unlike loan forgiveness, immediately stops your loan payments and may even allow you to receive a refund on your repayments.

To have your student loans discharged through borrower defense, you need to file a claim to the Department of Education with evidence that you were deceived or misled by your school.

Who Qualifies for Student Loan Forgiveness?

Eligibility for student loan forgiveness depends on the program being offered.

If you work in the public sector and have made enough qualifying payments, you may be eligible for the Public Service Loan Forgiveness program. On the other hand, if you are a teacher who’s worked for five consecutive years at a low-income school, you may be eligible for the Teacher Loan Forgiveness program.

If you feel that your career may qualify for loan forgiveness, be sure to check your eligibility with the Federal Student Aid office.

Closing Thoughts From the Nest

While the future of the Biden administration’s student loan relief program is still uncertain, you can subscribe to the Department of Education’s email updates to stay up-to-date with the latest information. Beyond Biden’s comprehensive loan forgiveness plan, remember there are still opportunities for you to have your federal student loans forgiven with existing programs.

If you are considering going to grad school after college, you may be wondering, “How much does grad school cost?”

Making the decision to attend graduate school is one thing, but paying for it is another issue. Whether you plan to take out graduate student loans, receive a scholarship, or pay out-of-pocket, being aware of the average cost of grad school and how it varies is important.

On Average, How Much Does Grad School Cost?

The average cost of tuition for public grad schools is roughly $30,000 per year, while private grad schools cost around $40,000 per year. However, these figures do not apply to specialized degrees in medicine and law, which usually cost significantly more.

While you are calculating the cost of grad school, be sure to think about the cost of attendance (COA), in addition to the tuition. The COA is the total amount of money you will have to pay to attend grad school, including tuition and other fees like transportation, room and board, school supplies, and more.

There is no “right” answer to the question of whether grad school is more expensive than undergrad, as the price depends on your field of study, type of degree, and other factors.

Generally, medical, law, and other specialized degrees cost more than an MBA or a Master of Arts. STEM degrees can also be pricier than a degree in humanities or social sciences, given that there may be additional costs in labs, equipment, and other materials.

Is Graduate School Worth the Price?

The question of whether grad school is worth the cost ultimately depends on your personal aspirations and financial standing.

Before making the decision, be sure to carefully weigh the pros and cons. Here are some things to consider:

Pros of Attending Grad School

More scholarship opportunities: Grad schools are usually more generous with their scholarship offerings than undergraduate programs are. If you take the time to find and apply for scholarships, you may be able to offset the cost of your tuition.

Career advancement: An advanced degree can unlock career doors for you that may not have been accessible with only a Bachelor’s degree.

Increased salary: The average salary of an individual with a Master’s degree is higher than the average salary of an individual with a Bachelor’s degree. By going to grad school, you can increase your earning potential.

Specialized study in the field you love: If you’re going to grad school, you are probably going to study something that you love and enjoy. By attending graduate school, you will be able to have an in-depth, specialized study of the field and become an expert.

Loss of opportunity to make more money: A majority of undergraduates decide to work in the industry after graduation. Going to grad school may be a potential loss of income that you could have made had you begun working instead.

Loss of time: Attending grad school can take anywhere from one to three years, in general, which may set you behind in comparison to your peers.

Potential student debt: If you don’t receive any financial aid or gift aid, you may need to take out graduate student loans to afford the cost of attendance. If you have previous debt from your undergraduate education, you may be shouldering even more student loan debt.

Delayed work experience: You may miss out on industry experience if you decide to go to grad school.

As with any degree, there is a certain order you should follow when it comes to how you finance your education.

Scholarships, fellowships, and grants are all forms of free aid, or gift aid. Typically, scholarships, fellowships, and grants do not need to be paid back, so you’ll want to accept these first.

After accepting any free money available to you, you should pursue work-studynext. Federal work-study is considered earned money, meaning you have to trade your time to receive it. While not everyone will receive federal work-study, it’s a great option for those who do.

Loans should always come last in the process because they are borrowed money. When you borrow a loan, it’ll typically accrue interest, and by the time you pay it back, you’ll have paid a significant amount in interest.

Attending grad school is a big decision to make. Be sure to reach out to current graduate students, academic mentors, and other role models who have been in your position before.

When it comes to financing the cost of your grad school tuition, be sure to consider all of your options. If you want to explore graduate student loans, consider submitting a free application with Sparrow. Sparrow allows you to compare your pre-qualified, private student loan options across 17+ different lenders.

Sparrow aims to give you the tools and confidence you need to improve your finances. Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. While we make an effort to include the best deals available to the general public, we make no warranty that such information represents all available products.

With average college tuition costs rising every year due to inflation, it’s increasingly important to be aware of the costs associated with higher education.

One aspect of this is understanding what exactly tuition is, along with how it differs across factors like geographical location and institution type.

Tuition vs. Cost of Attendance

Tuition and cost of attendance may seem like the same thing, but there is a significant difference between the two.

Tuition is the base amount of money you pay to attend the institution and take classes, while the cost of attendance is the estimated total of expenses you will pay as a student, which includes the cost of tuition, fees, and other student expenditures.

Cost of attendance = Tuition + Room and Board + School Supplies + Transportation Fees…

What is the Average Cost of Tuition in the US?

The average cost of tuition for a four-year, in-state, public institution is $9,377, while the average cost is $27,091 for out-of-state. For private institutions, the average cost of tuition for a non-profit is $37,641, while a for-profit costs an average of $18,244.

Average College Tuition by State

As you explore potential colleges, keep in mind that tuition can also be influenced by geographic region. Historically, public colleges in the northeast have been the most expensive, while the least expensive schools are in the Plains and the South.

The table below shows the average total cost of college tuition by state, ordered from greatest-to-list.

State

Tuition & Fees

Tuition + Room & Board

Vermont

$17,593

$30,752

New Hampshire

$16,749

$29,222

Illinois

$14,579

$26,252

Pennsylvania

$14,532

$26,040

Connecticut

$14,487

$28,425

New Jersey

$14,184

$28,335

Massachusetts

$13,939

$28,317

Virginia

$13,931

$25,761

Michigan

$13,716

$24,777

Rhode Island

$13,697

$26,946

South Carolina

$12,544

$23,181

Minnesota

$11,836

$21,858

Oregon

$11,537

$24,517

Arizona

$11,410

$24,681

Delaware

$11,343

$24,862

Kentucky

$10,976

$22,317

Alabama

$10,617

$20,993

Maine

$10,377

$20,677

Tennessee

$10,271

$20,639

Hawaii

$10,197

$22,012

Ohio

$10,049

$22,860

Indiana

$9,656

$20,572

Louisiana

$9,656

$20,031

Maryland

$9,401

$22,380

Iowa

$9,373

$19,788

Missouri

$9,310

$19,394

Colorado

$9,269

$22,288

Kansas

$9,081

$19,082

North Dakota

$9,065

$18,057

South Dakota

$9,012

$17,177

Alaska

$8,849

$22,185

Wisconsin

$8,782

$17,875

Nebraska

$8,761

$19,352

Mississippi

$8,642

$19,221

Arkansas

$8,468

$18,262

New York

$8,416

$24,231

California

$8,401

$24,015

West Virginia

$8,252

$19,312

Oklahoma

$8,064

$17,283

Texas

$8,016

$18,325

Georgia

$7,525

$18,711

Washington

$7,485

$21,027

Idaho

$7,482

$16,518

New Mexico

$7,393

$17,113

North Carolina

$7,260

$17,113

Montana

$6,993

$16,931

Utah

$6,764

$14,653

Nevada

$6,434

$18,065

District of Columbia

$6,152

N/A

Wyoming

$4,785

$14,584

Florida

$4,541

$15,543

Private vs. Public Schools

Public institutions are funded by the government, while private schools are funded by tuition and endowment funds.

Generally, private colleges have more expensive tuition than public schools. In the graph below, we can see that private four-year colleges have historically cost more than your average public four-year, public two-year, and private two-year school.

However, it’s important to note that the average cost of attendance differs from student to student.

A low-income student may receive more financial aid from private universities instead of public universities, given that several private universities are 100% need-based. On the other hand, it may be cheaper for an in-state, middle-income student to attend public schools instead of a private school, due to in-state grants.

All this is to say that you should explore your financial resources at every school you are interested in, public or private. Most schools offer an online tuition calculator that estimates what the total cost of tuition may be for your financial standing. Reach out to the financial aid office if you have any questions.

Closing Thoughts From the Nest

As you explore your college options, be sure to make note of the average undergraduate tuition for the institutions you are interested in. Whether you plan to borrow student loans or not, it’s important to be mindful of how much your education costs.

If you’re looking for private loans to finance your education, consider using Sparrow. Sparrow offers a free, online tool that allows you to compare pre-qualifying private loans across 15+ private lenders.

Both federal and private student loans can be used for educational expenses. While that typically means costs like tuition and fees, there’s a variety of items that fall under the umbrella.

In fact, you can use your student loans for living expenses, child support, and even study-abroad programs.

Can I Get a Student Loan to Cover Living Expenses?

Yes, you can use student loans for living expenses. After your student loans are disbursed to your school, your school will usually return the remaining funds to you after tuition, room/board, and other costs have been paid for.

These remaining funds can be used for a variety of expenses, such as institutional fees, transportation costs, and more.

What Counts as Living Expenses for Student Loans?

Any academically-related expense can be counted as a living expense for student loans. This doesn’t mean that you are strictly limited to purchasing school supplies or textbooks, however.

Your student loans cover living expenses you have to pay as a student, such as rent, bills, groceries, and even furniture for your campus apartment.

The following table outlines the most common expenses that student loans can be used for.

Expense

Tuition and Fees + Room and Board

Your institution will usually take a portion of your student loans to cover costs such as tuition and fees, room and board, and your meal plan. You will not have to pay the university directly. If you are opting for off-campus housing, your school will usually subsidize your rent up to the amount of housing costs you would have to pay if you lived on-campus. Your remaining student loans can be used to pay your bills.

Institutional Fees

If your school has mandatory health insurance, parking fees, or other fees, you can spend a portion of your student loans to cover these costs.

School-Related Living Expenses

Student loans can cover personal expenses that are necessary for your educational career. This includes groceries, new bed sheets, furniture for your apartment or dorm, and other living expenses.

Books and Supplies

Your student loans can cover anything from textbooks, notebooks, to a new book bag.

Transportation Costs

Whether you commute or drive to school, you can use a portion of your student loans to cover transportation costs like gas, bus fares, and other expenses.

Child Care Expenses

If you are supporting yourself in addition to a dependent, you can use your student loans to cover child care expenses, like daycare, baby food, and other child-specific necessities.

Study Abroad Expenses

If you decide to study abroad, you can use a portion of your student loans to cover any related expenses. Note that the study abroad must be either approved by or offered by your school to be a qualifying expense.

What Doesn’t Count as Living Expenses for Student Loans?

Any personal costs that are not absolutely necessary as a student do not count as living expenses. The following table outlines what you can’t spend your student loans on.

Expense

Entertainment

Movie tickets, ice skating tickets, and other forms of entertainment do not count as a living expense.

Clothes

Unfortunately, buying a new wardrobe does not count as a living expense that can be covered by your student loans.

Vacation/Travel

While a spring break trip to Bali would be nice, you can’t use student loans to cover it. Personal vacations and travel do not count as a valid living expense to use your student loans on. However, your student loans can be used for study abroad programs that are approved by or administered by your school.

Down Payments

You cannot use your student loans as a down payment to buy a new car, house, or equivalent.

Debt

While it might be tempting to knock out some credit card debt with your student loans, your personal expenses do not count as a living expense. However, if you paid for academic or necessary living expenses with your credit card, an exception can be made.

Is It a Good Idea to Use Student Loans for Living Expenses?

Generally, it is okay to use student loans for living expenses. However, you should consider the cost of doing so before making the decision.

Likewise, you’ll want to make sure essential academic-related expenses are covered before covering potentially non-essential living expenses with loans.

Leftover amounts from your student loans should be saved for future, unforeseen academic expenses like books for next semester or sudden charges to your bursar account.

You can consider other avenues for paying for your personal needs, such as picking up a new side hustle, tapping into your savings, or asking your parents for an allowance.

What Happens If You Use Student Loans for Something You Shouldn’t?

While no one is actively tracking what you spend your student loans on, you can face serious consequences if you’re caught for student loan misuse.

Using your loan funds improperly is essentially breaking a contract, as you agreed to use your loans for academic expenses only in your promissory note.